Abstract

The current crisis of the global monetary system forces the world community to search for ways of its reform. The focus is, first of all, on the issue of a qualitatively new international currency. In the context of this problem, a project is presented for the reincarnation of the Keynesian idea of an "objective standard of the value of a composite commodity", which in this case is the combined grain of the International Grains Council (IGC), with the aim of creating on its basis a supranational monetary unit GES (Grain Equivalent Standard) as an exchange rate benchmark /measure of value/ of national currencies plus for practical use as an international payment and reserve instrument. Since the movement of the market value of IGC grain is in the trend of the long-term movement of the value of the prevailing mass of commodity products, the new monetary architecture assumes, in essence, the binding of the GES currency to the general price trend of the world economy, which guarantees the stability of this currency in terms of purchasing power in the long term. – Guarantee of stability of global finances. Two options for reforming the global monetary system are proposed. The first option involves the creation of a global currency GES based on the weighted average value (in US dollars) on the world market of the IGC grain standard. – A symbolic currency, devoid of its own monetary base, is used as a measure of value and an international unit of account, an analogue of the SDR. The second option involves the creation of a global GES currency on its own monetary base, value-formatted by the global economy and attached to the weight of the IGC grain standard similar to the gold-dollar standard. – The currency is quite real, autonomous (independent of national currencies), used as a measure of value, a full-fledged means of monetary circulation, with the exception of bank lending. The first option involves linking the world currency to the market value of the IGC grain standard, the second – its direct value link to the weight of the IGC standard. Reforming the monetary system is designed to "anchor" national currencies (including the US dollar) on a solid material-value basis of the global economy, calm the emission-monetary bacchanalia in the world, stabilize the system of international settlements and payments, normalize equivalent commodity exchange in world trade, clearing pricing from pseudo-value falsity.

|

Published in

|

Economics (Volume 14, Issue 2)

|

|

DOI

|

10.11648/j.eco.20251402.11

|

|

Page(s)

|

22-33 |

|

Creative Commons

|

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited.

|

|

Copyright

|

Copyright © The Author(s), 2025. Published by Science Publishing Group

|

Keywords

Global Monetary System, World Monetary Unit, Supranational Currency

1. Introduction

The modern world economy is engulfed in a complex of financial and economic turmoil caused by the crisis of the world monetary system. A brief list of the most acute problems: a) huge deficits of state budgets, exceeding the critical 3% of GDP; b) the total debt in the world is three times higher than the world GDP; c) unrestrained emission of the money supply, which is several times higher than the normal rates of economic growth; d) fictitious capital of astronomical sizes: the volume of derivatives in the world economy is hundreds of trillions of dollars. These are the results of the dominant direction of financial policy in macroeconomics, the essence of which comes down to a massive injection of money into the economy to stimulate economic growth and counteract the crisis phenomena of cyclical development. In practice, this has led to a separation of the money supply from the material basis of real assets and a general disorder of the financial system.

The main vice of modern economic science is the lack of understanding of the value principles of money circulation. Hence the reckless course on "satisfying consumer demand" for money by unrestrained money emission, rapidly increasing the money supply in the economy. At the same time, the unbridled increase in the materially unsecured money supply in circulation gave rise to the so-called "financial economy": an increase in capital not in the sphere of commodity production, but through operations in the stock markets. The result is an incredible growth of fictitious capital, depleting the real sector of the economy. This is the result of the financial policy of the modern macroeconomic mainstream. The main reason for its viciousness is that the monetary system has no basis in the material-value of the real economy. As a result, world finances found themselves in a deep crisis after the liquidation of the gold-dollar standard of the Bretton Woods system, which was especially evident in 1998 and 2008.

Given the instability of the global financial system, there is a particularly acute need today for a radical reform of the global currency architecture – the creation of a qualitatively new international monetary unit as a reserve and payment means. This is necessary to curb emission-destructive processes in the economy, stabilize the system of international settlements, normalize equivalent exchange of goods in trade and overcome the pathological phenomena of the "financial economy". In this regard, we have proposed the idea of reforming the global currency system on the material and value foundation of the global economy, namely: based on the average weighted world value of the grain standard IGC (International Grains Council), it is proposed to create a supranational monetary unit GES (Grain Equivalent Standard), as an exchange rate benchmark (measure of value) for national currencies, an international payment and reserve means. The idea is not new. "Standard composite commodity" as an "objective standard of value" was proposed back in 1923 by J. M. Keynes in his "Treatise on Monetary Reform" (quote in the original language):

«

Professor Fisher's method may be adapted to deal with long-period trends in the value of gold but not with the, often more injurious, short-period oscillations of the credit cycle. Nevertheless, whilst it would not be advisable to postpone action until it was called for by an actual movement of prices, it would promote confidence, and furnish an objective standard of value, if, an official index number having been compiled of such a character as to register the price of a standard composite commodity, the authorities were to adopt this composite commodity as their standard of value in the sense that they would employ all their resources to prevent a movement of its price by more than a certain percentage in either direction away from the normal, just as before the war they employed all their resources to prevent a movement in the price of gold by more than a certain percentage. The precise composition of the standard composite commodity could be modified from time to time in accordance with changes in the relative economic importance of its various components»

.

As we see, Keynes proposes a "standard composite commodity" as an "objective standard of value". - Logical. The only thing would like to object to the venerable economist is that a standard is a standard in order to be constant, not change. The importance of Keynes's idea is that an objective standard of value of a composite commodity can become a very suitable material-value foundation for the creation of a qualitatively new monetary unit - supranational in this case. Let's take advantage of this opportunity.

2. The Labor-Value Essence of Money

So, the Keynesian "composite commodity" as a material standard of value is a kind of analogue of an ounce of gold. By the way, about gold. It is not by chance that Keynes suggests abandoning the "gold standard". In the era of rapid economic development, it is absolutely unsuitable to be a standard of value. There are two reasons for this: a) gold production significantly lags behind the rate of economic growth, which, under the conditions of the fixed value of the "gold standard", inevitably leads to a liquidity crisis and a slowdown in economic development; b) a very large subjective-emotional component in the formation of the market price of this mineral, which significantly distorts its real value (the volatility of gold stock exchange quotations since 1972 speaks for itself

). Consequently, money was doomed to break away from the "gold standard" and, in the form of a value denomination on the corresponding media, move into free floating... But where to? The question remains open to this day, since the prevailing belief in economic theory is that money is a means – any product, good, object, asset – for market exchange and payments. Is such a definition of money satisfactory? – Doubtful. Such a definition of money provokes the desire to turn on the “money production” machine at full power to increase GDP (partly it is). So, let us once again define the true essence of money.

First of all, money is an expression of the labor intensity of goods - the nominal value on certain media as an imaginary image of the labor actually spent on their production. We are talking specifically about the objective labor intensity of commodity products, and not their subjective-capricious utility, which is influenced by the variability of consumer preferences. The monetary instrument of exchange serves the circulation of labor costs (live - embodied) in the economy, and not the circulation of ephemeral-emotional utility in the minds of people. Money is a symbolic-sign representative not just of goods (items, objects, assets), but of their value as a market assessment of the labor intensity of these goods. After all, in commodity exchange, it is the value proportions of goods that are compared by their labor intensity, and not their volume or weight, and the influence of utility on pricing is effective only until the moment of equilibration of the value at the average rate of profit from the sale of goods, then it disappears. Therefore, modern money is by no means a “specific commodity” (“wealth”, according to Friedman

), since as symbolic-sign carriers it does not have its own value, it only represents it. Even under the “gold standard”, gold, which was used as commodity money, was nothing more than a carrier of value, and it was exchanged for all other goods in the same value proportions. Commodity money in the form of gold or silver is a direct carrier of real value. Paper money is a nominal representative of the value of the same gold or silver. Another matter is whether the value denomination of paper money corresponds to the real value of these minerals, as well as other material goods. Given the abnormal volatility of the gold market price, it clearly does not meet the requirements of the value standard of modern money. Therefore, we turn to the value of a combined commodity according to Keynes's recipe.

3. IGC Grain as a Material Standard for the Formation of the Nominal Value of the GES Currency on Its Basis

Let us specify the Keynesian definition of a “standard composite commodity”: what composite commodity can become the material basis for the formation of a sub-standard value? The first thing that comes to mind is the FAO UN food basket, the value of which is the basis for calculating the world food price index: “Food Price Index: Consists of the average of 5 commodity group price indices (meat, dairy, cereals, vegetable oil and sugar); in total 73 price quotations”

. When mentioning 73 quotations, the question arises: is it necessary to take the entire set of components of the FAO basket as a food standard of cost? After all, more does not mean better. You can take, for example, the most significant part of this basket in the form of a grain product of the International Grains Council (IGC), which, in particular, includes feed grain for feeding livestock and poultry

. In any case, a comparison of the price trends of the IGC and FAO will only be beneficial. IGC statistics have been kept since 1949, and FAO has been using them since 1961.

What are the advantages of a grain standard for the formation of a sub-standard of the value of a supranational monetary unit on its basis?

Firstly, it is a product of unchanging quality, which existed in the past and will exist in the future. Secondly, it is a product of prime necessity, the most widespread in all latitudes of the globe. Thirdly, it is a purely labor origin of the grain product: labor and only labor. Fourthly, it is stable in human consumption regardless of social status: in bread consumption, everyone is equal - both rich and poor. Fifthly, the bread product is completely devoid of the emotional component of demand for it, only a physiological need for it: according to WHO UN, the daily consumption rate is 330 g per person - 120 kg per year

; taking into account feed grain for feeding livestock and poultry - 300-342 kg per person per year

. The stability of bread product consumption in developed countries is striking: in the USA

and Europe

. Sixth, grain is not an attractive object of financial scams and speculations, it is not subject to the opportunistic influences of stock market panic (like gold). Seventh, the stability of supply and demand for many decades: grain production increases exponentially with population growth, regardless of economic crises and social upheavals

. The law of value (where it operates), promptly responding to demand, adjusts production volumes to it through the timely transfer of capital to the industry up to the average rate of profit. Yes, weather and climate conditions... However, grain yields in the world, despite the vagaries of nature, are steadily growing

| [11] | Hawkesford M. J., Araus J. L., Park R. Food and energy security. Figure 1: Progress in world average yields for major cereal crop yields. Data from FAOSTAT. Wiley Online Library. 2013. Mar 12. https://doi.org/10.1002/fes3.15 |

[11]

. Plus, year after year, world grain reserves are constant within 20-40% of gross production

. World demand for grain products has been generally balanced with its supply over the past 60 years

, which is the key to the correct formation of the value of the product: nothing but "cost price + average profit". The grain price trend on world markets in recent decades has been distorted mainly by the off-market formation of oil prices

. And this is despite the striking synchronicity of population growth, grain production and oil extraction

, which, it would seem, should have reduced the volatility of the grain price trend to a minimum.

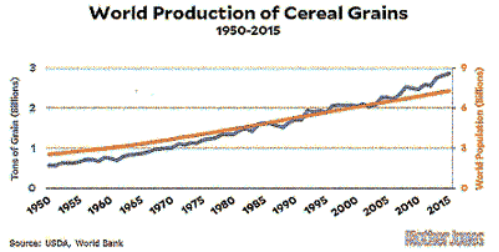

The main thing in pricing is the balance of supply and demand at the average rate of profit from its production. This is how the optimal price is set. According to the US Department of Agriculture and the World Bank, for the period 1950–2015, there has been a virtually synchronous growth in global grain production in relation to the numerical growth of the world's population (

Figure 1)

, which guarantees the stability of the balance of supply and demand for this product - the key to its optimal pricing.

Figure 1. Synchronicity of growth in world grain production to population growth, 1950–2015.

The pricing of commercial grain on world markets is determined by the law of value: the price of production costs (cost price) + average profit under conditions of general equilibrium of supply and demand. With such a synchronous (with some advance) growth of world grain production to the growth of the planet's population, there should have been a linear price trend for grain. However, the cataclysms of the First and Second World Wars, the Great Depression of 1929-1933, the price shock of the energy crisis of the 1970s and the surge in off-market oil prices in the period 2004-2014 significantly distorted the pricing trend for grain products

. The same applies to prices for industrial raw materials

. Nevertheless, the general trend of a decrease in prices on a global scale is obvious.

According to the OECD and FAO, “over the past 100 years, real prices of wheat have fallen by an average of 1.5% per year. Similar patterns are observed for other commodities” (

Figure 2)

.

Figure 2. The long -term trend of reducing the cost of wheat (in real prices) in 1908–2016, dollars /t.

“Real maize prices have been declining over the period 1908–2016,” the OECD and FAO continue to note, “with the average price falling by 1.5% per year in real terms. Similar trends are observed for other commodities” (

Figure 3)

.

Figure 3. The long -term trend of reducing the cost of corn (in real prices) in 1908–2016, dollars /t.

According to FAO, the same downward price trend applies to other cereals, including rice, as well as a decline in the overall food price index

.

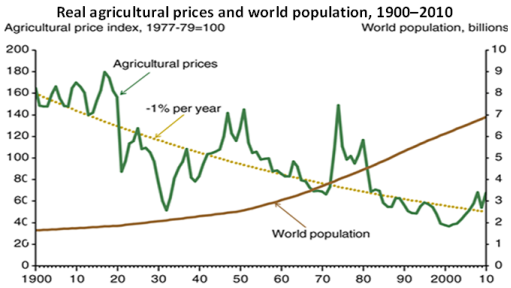

The United States Department of Agriculture (USDA) insists on almost the same figures: “In inflation-adjusted U.S. dollars, agricultural prices fell by an average of 1% per year from 1900 to 2010, despite the world’s population growing from 1.7 billion to 7 billion people during the same period” (

Figure 4)

.

Figure 4. A decline in real prices for agricultural products against the backdrop of a growing world population.

Source: USDA. Economic Research Service. Depicted in the chart is the Grilli-Young agricultural price index adjusted for inflation by the US GDP implicit price index. The Grilli-Young price index is a composite of 18 crop and livestock prices, each weighted by its share of global agricultural trade. World population estimates are from the United Nations.

Source: USDA. Real agricultural prices have fallen since 1900, even as world population growth accelerated. 2012.

.

As we can see, the decline in prices (%) for wheat and corn, on the one hand, and for agricultural products in general, on the other, over the past 100 years is quite comparable. As for the general decline in prices for raw materials for the manufacturing industry, IMF experts, based on data from The Economist magazine, analyzing the dynamics of prices from 1862 to 1999, note "a trend of a decline in real prices for industrial raw materials by 1.3% per year over the past 140 years" (

Figure 5)

.

And here we see a proportional synchronicity of the fall in real prices for grain crops and raw materials for the manufacturing industry by a comparable percentage. That is, the value of products of constant quality, which includes grain, is slowly drifting downwards somewhere within 1-1.5% per year in the long term. It must be assumed that a similar trend of a general decrease in value by a corresponding percentage concerns the prevailing mass of goods in general. How can such a downward price trend be explained? There are two reasons for its formation.

1) The growth of labor productivity in the world, which determines:

a) the growth trend of the world gross product in terms of goods and value;

b) the general trend of lower prices due to the reduction in production costs.

2) The growth of the world population.

The general trend towards lower prices is determined by the growth of labor productivity due to the reduction in production costs and the increase in the mass of the manufactured product. But the growth of the world population slows down the rate of price reduction, because consumer demand is increasing. The entire set of these factors forms a long-term price trend of the world economy towards a reduction in the value of commodity products (we see this on the Figure 2, 3, 4.

5). Unfortunately, the linearity of the trend has been significantly distorted by the voluntarism of oil pricing over the past half century

. Let's hope that this is a temporary phenomenon.

Thus, food grain, as the product most in demand by consumers, is the best "candidate" for the role of a material standard for the formation of a standard value on its basis, given that the downward trend in its value is characteristic of the movement of the value of the prevailing mass of commodity products. The pricing of grain products is in the general downward price trend of the global economy. This is exactly what is needed for the stability of the monetary unit in terms of its purchasing power in the long term, if the average weighted value of the standard grain is taken as the basis for this unit, taking into account the decrease in its price. For such a monetary unit, it will be possible to buy the same amount of goods for decades. This is exactly what a stable monetary system requires, in this case, a global one. Consequently, there is every reason to talk about the grain standard of value as the basis of a supranational monetary unit.

The stability of the purchasing power of the international currency is the main condition of global financial stability. What is financial stability in practice? In real life, it is a financial state in which the accumulated funds will be fully preserved for 10-20 years or more, and the issued/taken loan will be fully repaid after 10, 20 or more years. We are talking about the unshakable stability of the monetary unit in terms of purchasing power in the long term. Trust in money is the key to financial stability. This is the most important thing for doing business, for planning it, for implementing business projects. This is urgently required by both households and large companies. This is required by international economic relations. The stability of the purchasing power of the monetary unit should be the basis for the new currency architecture. How to implement this?

If there were no economic growth, there would be no need to adjust the nominal value of money. Humanity could still be content with the "gold standard". However, in our age of rapid economic development, such an adjustment is unavoidable. How to maintain the stability of the purchasing power of a monetary unit? The answer is through measured money emission, focusing on the percentage of the general price level decrease in the long-term trend. It is necessary to produce a measured emission, without reacting to any cyclical or random fluctuations in the economy. If the long-term price trend demonstrates an annual decrease by an average of 1-1.5%, then, accordingly, the money supply should be emitted by the same percentage from year to year, without paying attention to the market situation. In order to depreciate (devalue) the monetary unit by additional emission synchronously with the decrease in the price of the grain standard by the same percentage, thus maintaining its purchasing power. The general trend of cheapening money should coincide with the general trend of cheapening goods. This is a guarantee of stability of both the monetary system and global finances as a whole. Is the implementation of such a requirement sufficient in modern conditions?

Looking at the graphs above, we notice some slowdown in the rate of price decline in the 21st century, caused by the sharp jump in the price of crude oil since 2004

.

The price of oil, like any other goods, should be formed by a market according to the law of value: the price of production costs (cost price) + average profit. In reality, we see how the voluntarism of the owners of this resource distorts all pricing in the global economy. The correlation of food prices from oil prices is very obvious: «Oil and food prices are strongly correlated (93.4%)»

. Therefore, reforming the world monetary system in such conditions is very problematic. Nevertheless, it is desirable to prepare for such reform. After all, the instability of the currency system is one of the reasons for the rise in oil prices. The introduction of a stable supranational currency should reassure the world market.

Thus, a supranational currency should be guided by the general price trend of the global economy. Not by gold, not by the growth of global GDP, not by the total price of all goods and the velocity of money circulation (according to the Fisher formula), but by the general trend of price movements in the world in the long term. This is what guarantees the stability of the purchasing power of the currency and ensures the stability of global finances.

4. Supranational Currency GES Based on the Market Value of the Grain Standard IGC

As we have already found out, the world price of food grain is in line with the general price movement in the world and drifts freely with it. By linking the nominal value of the monetary unit to the value drift of this grain, we will obtain its stability in purchasing power in the long term, stability of world finances. Therefore, as the value basis of the supranational currency, we take the weighted average value of grain of the International Grains Council – IGC

. Moreover, to simplify the calculations, we can limit ourselves to three main grain crops - wheat, corn, rice. Corn makes up about 40% of all grain; wheat - about 30%; rice - about 20%. The share of all of them together accounts for almost 90% of all grain production

. There are two options for reforming the world currency system based on the market value of the IGC grain standard.

4.1. Reform Option One: GES Currency as a Benchmark for National Currencies, International Monetary Unit of Account

The algorithm for calculating the value of the IGC grain standard and creating the GES monetary unit on its basis is as follows.

1) We take 1 ton of combined IGC grain (wheat, corn, rice in proportions of production and consumption) and establish it as a material-standard foundation of the monetary unit - a grain analogue of an ounce of gold.

2) We fix the average world price of the basic standard "1 ton of IGC grain" over a certain period (10-20 years) as a monetary substandard of value in dollar terms. We get a grain-dollar standard - an analogue of the gold-dollar standard (Gold and Exchange Standard). With the difference that there the dollar was tied to the weight of the material (gold) standard, and here - to the market value of the material (grain) standard.

3) Based on the dollar sub-standard of the value of the IGC grain standard (according to Keynes: objective standard of value of a standard composite commodity), we approve the supranational currency GES (Grain Equivalent Standard):

1 ton of IGC grain → IGC grain exchange price (in USD) → monetary unit 1 GES.

That is, we create a world currency based on the market value of 1 ton of IGC grain according to the algorithm:

STANDARD of commodity → SUBSTANDARD of value (in USD) → currency 1 GES.

The monetary unit formed in this way acquires a value scale of prices, that is, it receives a nominal value link to the real value of a fixed particle of material goods in the form of a standard 1 ton of grain IGC:

Currency 1 GES = market value of 1 ton of IGC grain.

From this moment on, the GES currency unit begins to live its own life, being directly tied only to the market value of the IGC grain standard, and the exchange rate of national currencies, including the dollar, is oriented towards the grain-currency standard in the form of the GES currency unit. This is a symbolic currency unit in non-cash form, an analogue of the SDR, but based not on floating exchange rates, but on the market value of a real material good. The GES currency is artificially created, deprived of its own monetary base (for the market equation “1 GES = 1 ton of IGC grain” it is practically impossible to create such a base), but it is possible to create a monetary base for it from other currencies that adhere to the GES standard. The priority function of the GES currency is to be a measure of the nominal value of other currencies; its main task is to calm the emission bacchanalia in the world and become a value standard for settlement transactions of exchange, payments and savings.

In order to maintain the GES currency rate (in relation to the declining market value of the IGC grain standard), its nominal value must be annually devalued in sync with the decline in the value of the standard grain by 1-1.5% by symbolic emission. Real money emission is carried out by the currencies of the GES zone participants by the same percentage. The weighted average price of “1 GES = 1 ton of IGC grain” should remain stable on the world market for a long time – several decades. The regime of annual monetary emission by 1-1.5% must be strictly observed, regardless of fluctuations in the world economy, for at least a decade. Every 10 years, the world market weighted average price (in GES currency) of the IGC grain standard is revised and the GES currency emission percentage is adjusted. The main goal of the correction is the stability of the purchasing power of the currency in the long term.

The initiative to create a GES currency should come from the International Monetary Fund and can be used by it in two ways:

a) as an “anchor” for SDR, i.e. a rigid link between SDR and GES standard;

b) implementation of GES instead of SDR, rebasing of the IMF from SDR to GES.

In both cases, the organizational structure and functions of the IMF do not change. Only the monetary configuration system changes: either the SDR is stabilized by being linked to the GES standard, or the SDR is replaced by the GES. The advantage of the GES over the SDR is only in one thing - a solid support for the material-value foundation of the world economy, which the SDR does not have.

Today, if, for example, it were necessary to introduce the Grain Equivalent Standard, the nominal value of its currency in US dollars would be approximately in the range of 200-250 dollars per 1 GES, according to rough estimates based on the statistics of the International Grains Council, taking into account the average weighted price of IGC grain components in the world market in the proportion of production and consumption over the past 10-20 years. However, in this case, we should not forget about the abnormally high (excessive to the costs of production) price of crude oil since 2004 and its volatility, which significantly distorted grain pricing. Plus COVID and Russian aggression against Ukraine. Therefore, this is not the best time for reform.

4.2. Reform Option Two: GES Currency as a Benchmark for National Currencies, a Full-fledged Payment and Reserve Instrument

The algorithm for creating a full-fledged GES monetary unit based on the market value of the IGC grain standard looks like this.

N-quantity of banknotes are massively injected into the world economy, distributing them among countries in proportion to their population size. Any number of monetary media. Taking into account the forthcoming linking of this money supply to the GES standard, we can take, for example, the symbolic number of 3 billion banknotes, which is comparable to the annual grain harvest in the world in tons (the world grain harvest is almost 3 billion tons per year). Or we can issue 400-500 billion banknotes, which is comparable to the estimated world GDP in GES currency (dividing 100 trillion dollars of the current world GDP by the average weighted world price of grain IGC within 200-250 dollars per ton). The initial number of banknotes is not of fundamental importance. It is better to take more, so that later there is no need to divide the GES monetary unit into mili-GES, micro-GES, nano-GES...

So, throw this multi-billion dollar mass of banknotes into the world economy as the future monetary base of the GES currency. And... we pause. Let it (this monetary base), absolutely freely rotating in the world economy, live its own life - a year, two or three, or maybe more. Without any external influence on it. So that the global economy itself formats this freely rotating money supply in value, calibrating the value denomination of the monetary unit, assigns it a real price. And then, when after a series of inevitable fluctuations the nominal value of the thrown currency stabilizes and we see the real price of the IGC grain standard in this currency, we will only have to formally formalize the monetary reform. In this case, the algorithm for forming the GES currency unit will have the opposite direction and with the sign "=" between the nominal value of the currency and the real value of the standard, which means a direct value linkage of the denomination of 1 GES to the reference weight of the IGC grain. That is, the sub-standard of value in the GES currency of the IGC grain standard (according to Keynes: objective standard of value of a standard composite commodity) is the currency of 1 GES.

Currency 1 GES = SUBSTANDARD of value (in GES currency) → STANDARD of commodity.

This time, the 1 GES currency will determine the IGC grain reference weight for itself. It is unlikely to be 1 ton of the grain reference. However, this is not of fundamental importance. The main thing is the solidity of the material-value basis under the GES currency. The monetary unit formed in this way acquires a value scale of prices, that is, it receives a nominal-value link to the real value of a fixed particle of material goods in the form of the IGC grain reference. – A complete analogue of the gold-dollar standard GES (Gold and Exchange Standard), with the difference that there the price scale “$1 = 0.88571 grams of gold” was legislatively fixed by the subjective decision of the participants of the Bretton Woods conference, and here the price scale “1 GES = reference weight of grain IGC” is objectively determined by the economy itself. And there was a rigidly fixed scale of prices for the monetary unit, but here it is freely floating (drifting) in the general price flow of the global economy.

Currency 1 GES = market value of a fixed (in kg or t) particle of IGC grain.

From this moment on, the GES monetary unit begins to live its own life, being directly tied to the market value of the IGC grain standard, and the exchange rate of national currencies, including the dollar, is oriented toward the grain-currency standard in the form of the GES monetary unit. This will already be a full-fledged monetary unit, as a measure of the nominal value of other currencies, based on its own monetary base, actually performing the function of a payment and reserve means in international economic relations. A real currency (in cash), created by the economy itself. Its main task is to calm the emission bacchanalia in the world, to become a full-fledged instrument of financial transactions of exchange, payments and accumulation.

To maintain the rate of the new currency (in relation to the declining market value of the IGC grain standard), the GES monetary unit must be devalued annually by 1-1.5% by measured money emission, increasing the monetary base by the same percentage (taboo on credit emission, only monetary base). The weighted average price “1 GES = IGC grain reference weight” should be stable on the world market for a long time – several decades. The regime of annual money emission by 1-1.5% must be strictly observed, regardless of fluctuations in the world economy, for at least a decade. Every 10 years, the weighted average price of the IGC grain standard on the world market is revised and the percentage of GES currency emission is adjusted. The main goal of the correction is the stability of the purchasing power of the currency in the long term.

It is desirable that the initiative to create the GES currency be put forward by the International Grains Council (in which, by the way, the Saudis are present, who must be extremely interested in the long-term stability of the world currency in order to preserve their monetary assets) with the support of the UN. The role of issuer and regulator of the GES currency can be taken on, for example, by the World Bank or the Bank for International Settlements. That is, authoritative international institutions. The higher the authority, the more trust.

The initial stage of the implementation of this reform project can be started in the near future, by introducing into the circulation of the world economy a certain mass of authoritative GES monetary signs to “warm up” (prepare) this money supply for the future installation of the Grain Equivalent Standard, as soon as the nominal value (price) of the GES monetary unit stabilizes.

The absolute autonomy of the GES currency, its independence from anyone’s emission whims, is an undeniable advantage of the second version of the reform over the first. But there is a common advantage to both options. Unlike gold and other assets, in times of economic instability no one will rush to panic buy grain or sell it (this is physically impossible), which minimizes the volatility of pricing for this product. Especially if speculative futures trading with grain commodities is prohibited. The stability of the weighted average price of the IGC grain standard is the key to the stability of the GES currency.

4.3. The Simplest and Most Illusory Path to Reform

So, we have considered two options for reforming the world currency system based on the Grain Equivalent Standard. Each option has its advantages and disadvantages. There is another option for reforming, the simplest one, because the entire modern financial infrastructure is built for it. This refers to linking the American dollar to the GES standard. In this case, the US Federal Reserve System will need to moderate its unbridled emission ardor, agreeing to dollar emission of no more than 1-1.5% per year with the simultaneous introduction of a 100% bank reserve rate to tame the multiplier of credit and money emission. It is hard to believe, despite the fact that such a decision by the Fed would restore general confidence in the American dollar. Such a reform would only simplify the grain-currency system, limiting the GES standard to the function of a measure of value and reducing its role mainly to an exchange rate benchmark for national currencies. At the same time, the normalization of equivalent exchange of goods in world trade on the basis of the grain-dollar standard, the establishment of justice in international settlements and payments, the cessation of the export of inflation by excessive emission of the dollar outside the United States - all this would satisfy the passions around the question of "who is robbing whom?" and would reduce the degree of hatred towards the United States.

5. The Role and Importance of the World Monetary System GES

The peculiarity of the GES system is the presence of a value scale of prices, that is, the binding of the monetary unit to the value of the reference particle of a material good, which is IGC grain. The material standard is rigidly fixed in the weight of IGC grain: 1 ton - according to the first option; according to the second - so far "?" kilogram or tons. But the value of the grain standard freely drifts in the mainstream of the movement of the value of the main mass of commodity products downwards. Accordingly, the price scale of the GES system freely drifts in the general flow of value on the world market, synchronously to it, in unison with it. - The key to the long-term value adequacy of the GES currency is on the basis of its organic binding to the value foundations of the real economy. This is a significant advantage of the grain currency standard over the gold currency standard, where the price scale was rigidly fixed in the parameters of 35 dollars. per troy ounce (0.88571 g of gold per dollar), without taking into account the trends in the movement of the market value of the gold standard, which doomed the dollar to isolation from the value foundations of the economy. But even if the dollar were tied to the market value of gold (and not to its weight), the gold exchange standard would not stand the test of practice, since gold is unsuitable as a value standard for the reasons mentioned above. As for the modern system of Special Drawing Rights (SDR), the price scale as such does not exist for it at all. The dollar to SDR exchange rate ($1.3 = 1 SDR as of February 2025) says little about the value parameters of currencies, since the dollar itself has been deprived of a price scale since August 15, 1971.

The synchronous reduction in the value of the IGC grain standard in line with the general reduction in the value of the main mass of commodity products should guarantee the value stability of the GES currency unit for the long term: the purchasing power of 1 GES will remain unchanged in 10 years, and in 20 years, and beyond. This is the main thing that is necessary for the stability of the international monetary system. Of course, subject to the nominal correction of the GES currency according to the downward drift in the value of the IGC grain standard due to additional money emission by the corresponding percentage. That is, there must be an emission correction of the monetary unit in time with the decrease in the consolidated price index for the grain components of the IGC standard. In order to devalue the monetary unit proportionally to the downward price index, thus maintaining the stability of the purchasing power of the GES currency. If, for example, the IGC reference grain in kind were (let's hypothetically imagine such a variant) a monetary unit, like gold or silver coins, such an adjustment would be superfluous. But since money is only a nominal representative of the value of the specified grain, and does not have any value as such, then the adjustment is inevitable.

The GES currency, due to the fixed price scale of its unit, must determine the true price (exchange rate) of national monetary units, revealing their possible pseudo-value deviations. If, for example, in 10 years it suddenly turns out that the nominal price of 1 ton of the IGC grain standard in dollar terms is not the same as it was at the time of the approval of the GES standard, but somewhat higher, one of two reasons for the price distortion remains: either the Fed turned on the printing press, or, most likely, launched the credit emission multiplier. The same applies to other national currencies. This, of course, disciplines the monetary policy of central banks, forcing them to observe money-value parity, that is, to adhere to zero inflation/deflation.

In addition, by qualitatively performing its main function as a measure of value, the new monetary system will significantly simplify the calculation of value parameters when implementing financial exchange transactions, payments, accumulation, making unnecessary the need for such instruments for calculating inflationary distortions of value movement as the GDP deflator and the consumer price index. The value adequacy of the GES currency will make it possible to more accurately calculate the macroeconomic parameters of the gross product and national income. Consequently, there will be no problems with the applied functions of money if the GES currency qualitatively performs its function as a measure of value. The positive result of the introduction of the GES currency will be that financially inflated assets that have no real value will be revealed, and the fictitious over-accumulation of capital will be put to an end. If there are some risks in the introduction of the new currency system, then only with a plus sign.

Today, the dollar still holds the status of a global currency, but this cannot continue indefinitely, especially considering the astronomical US national debt as a time bomb under the entire dollar system. If the dollar has not yet left the pedestal of the dominant currency, it is only because it currently has no alternative. "The dollar is used as a global currency for reasons that make it difficult for other countries to find an alternative with the same properties"

, says US Secretary of the Treasury J. Yellen. At the same time, due to the growing mistrust of the American currency, centrifugal processes of deglobalization and economic fragmentation are growing. As more and more countries leave the dollar zone, the US will lose its hegemonic advantage in the global monetary system. "The trend towards de-dollarization of gold and foreign exchange reserves in the world will continue"

, assure IMF experts.

In conclusion should be noted. In the modern globalized world, it is impossible to create a nationally isolated oasis of financial stability based on a national currency. The USA, China, and the European Union can somehow afford it, but nothing more. All possible attempts to build an economically prosperous economy in a separate country based on a national currency will inevitably be brought to naught by globalization processes. Autonomous creation of national currencies in modern conditions is futile. The global economy requires the presence of a supranational currency as an exchange rate benchmark for national currencies, and which itself would perform the function of a payment and reserve means.

6. Conclusions

The practice of recent decades proves that the basis of the world currency system should not be the ephemeral value of gold or floating rates of national currencies, but reliance on the labor-cost essence of material wealth. The shortcomings of the gold and foreign exchange standard GES led to its liquidation in the 1970s, quite justifiably. And SDR did not get rid of these shortcomings. Since then, the world currency system has been "homeless" - deprived of support on the material-cost basis of the real economy, therefore, it is on the verge of destruction. Hence, by the way, the crypto-currency perversions of modern finance are already a pathology. Fiat money is a priori a fiction (the author's conviction). Therefore, today the task is to find a new supranational monetary unit, for which we propose the GES currency.

The main advantage of the grain GES standard is that the value basis of its currency, based on the material foundation of the world economy, freely drifts in line with the general trends of the movement of the value of the overwhelming mass of commodity products towards a decrease. That is, in essence, the supranational currency is tied to the long-term price trend of the global economy. This is the guarantee of the stability of the GES monetary unit in terms of purchasing power for the long term, a guarantee of the stability of the supranational monetary system.

The practical task of the Grain Equivalent Standard is to anchor national currencies (including the US dollar) on a solid material-value basis of the global economy and to calm the emission-monetary bacchanalia in the world. This is required for the stabilization of international settlements and payments, the normalization of equivalent exchange of goods in world trade. Finally, to ensure the development of the real sector of the economy, clearing pricing from pseudo-value falsity and taming the self-expansion of fictitious capital. All this is possible with the presence of value adequacy of the supranational monetary unit.

Abbreviations

IGC | International Grains Council |

GES | Grain Equivalent Standard |

SDR | Special Drawing Rights |

GDP | Gross Domestic Product |

FAO | Food and Agriculture Organization |

WHO | World Health Organization |

OECD | Organisation for Economic Co-operation and Development |

USDA | United States Department of Agriculture |

IMF | International Monetary Fund |

Author Contributions

Volodymyr Ognevyi is the sole author. The author read and approved the final manuscript.

Conflicts of Interest

The author declares no conflicts of interest.

References

| [1] |

Keynes J. A Tract on Monetary Reform. Gutenberg. 1923. URL:

https://www.gutenberg.org/files/65278/65278-h/65278-h.htm

|

| [2] |

Gold price from 1970 to 2023. Goldomania. URL:

https://goldomania.ru/menu_003_002.html

[in Russian].

|

| [3] |

Friedman M. Quantity Th eory of Money. Economics. URL:

https://www.economics.kiev.ua/index.php?id=49&view=article

(accessed on: 16.10.2023) [in Russian].

|

| [4] |

World Food Situation: FAO Food Price Index. Monthly Bulletin of Statistics. 2023. Jun 16. URL:

https://unstats.un.org/unsd/mbs/app/mbsnotes.aspx?tid=55

|

| [5] |

World Food Situation. Table: FAO Food Price Index. Food and Agriculture Organization. 2023. Jun 02. URL:

https://www.fao.org/worldfoodsituation/foodpricesindex/en/

|

| [6] |

Makhynko V. Makhynko L. Bread consumption norms in diff erent countries of the world from the perspective of meeting the body’s needs. DocPlayer. 2017. URL:

https://docplayer.net/41416647-Normi-spozhivannya-hliba-v-riznih-krayinah-zpoglyadu-zadovolennya-osnovnih-potreb-organizmu-mahinko-v-m.html

(accessed on: 19.05.2018) [in Ukrainian].

|

| [7] |

Vishnevskiy A. Is it possible to feed the whole world? Val-s.narod. URL:

https://www.val--s.narod.ru/gl_visnevsky.htm

(accessed on: 21.04.2018) [in Russian].

|

| [8] |

Shahbandeh M. Per capita consumption of wheat fl our in the U.S. 2000-2023. Statista. 2023. May 15. URL:

https://www.statista.com/statistics/184084/per-capita-consumption-of-wheat-fl our-in-the-us-since-2000/

|

| [9] |

Wunsch N.-G. Average bread and bakery consumption volume per capita in Euro pe from 2010 to 2023. Statista. 2023. Jun 27. URL:

https://www.statista.com/statistics/806333/europe-bread-and-bakery-production-volume-by-category/

|

| [10] |

Speight A. Are geo-politics constraining food? Grain market daily. Figure USDA: With the agricultural growth grain production has risen with population. AHDB. 2021. Oct 08. URL:

https://ahdb.org.uk/news/are-geo-politics-constraining-food-grain-market-daily

|

| [11] |

Hawkesford M. J., Araus J. L., Park R. Food and energy security. Figure 1: Progress in world average yields for major cereal crop yields. Data from FAOSTAT. Wiley Online Library. 2013. Mar 12.

https://doi.org/10.1002/fes3.15

|

| [12] |

Jamieson C. The IGC Offers a Glimmer of Hope for 2016/17 Wheat Markets. Progressive farmer. 1/21/2016. URL:

https://www.dtnpf.com/agriculture/web/ag/blogs/canada-markets/blog-post/2016/01/21/igc-offers-glimmer-hope-201617-wheat

|

| [13] |

World grain and oilseed supply and demand v ending stocks 1960 to 2012. Source USDA. Moffi ttsFarm. 2019. Nov 11.

https://www.moffittsfarm.com.au/2013/08/21/world-food-production-and-outlook/world-grain-and-oilseed-supply-and-demand-v-ending-stocks-1960-to-2012-source-usda-via-anz-813/

|

| [14] |

Oil and food prices. Globalagriculture. 2020. URL:

https://www.globalagriculture.org/transformation-of-our-food-systems/book/infographics/oil-and-food-prices.html

|

| [15] |

Chefurka P. How Tight is the Link Between Oil, Food and Population? Figure: Grain, Oil and Population 1985 to 2007. Permaculture Research Institute. 2013. Feb 02. URL:

https://www.permaculturenews.org/2013/02/02/how-tight-is-the-link-between-oilfood-and-population/

|

| [16] |

Drum K. Did Population Growth Drive Conflict Growth After World War II? Mother Jones. 2017. April 18. URL:

https://www.motherjones.com/kevin-drum/2017/04/did-population-growth-drive-conflict-growth-after-world-war-ii/

|

| [17] |

Inflation-adjusted price indices for corn, wheat, and soybeans show long-term declines. Ers.usda. 2019. Apr 23. URL:

https://www.ers.usda.gov/data-products/chart-gallery/chart-detail?chartId=76964

|

| [18] |

Commodity prices are close to the bottom of the cycle. Figure: Commodity-prices index, industrials. Th e Economist. 2014. Jan 09. URL:

https://www.economist.com/graphic-detail/2014/01/09/more-valleys-than-hills

|

| [19] |

OECD-FAO Agricultural Outlook 2016-2025. OecdiLibrary. 2015. URL:

https://www.oecd.org/content/dam/oecd/en/publications/reports/2016/07/oecd-fao-agricultural-outlook-2016-2025_g1g66608/agr_outlook-2016-en.pdf

|

| [20] |

OECD-FAO Agricultural Outlook 2017-2026. OecdiLibrary. 2016. URL:

https://openknowledge.fao.org/server/api/core/bitstreams/1632705b-bb8e-4966-8c0a-6a63b3bac836/content

|

| [21] |

Prospects for aggregate agriculture and major commodity groups. FAO. URL:

https://www.fao.org/4/y4252e/y4252e05.htm

|

| [22] |

Real agricultural prices have fallen since 1900, even as world population growth accelerated. USDA. 2012. Nov 07. URL:

https://www.ers.usda.gov/data-products/charts-of-note/chart-detail?chartId=76174

|

| [23] |

Cashin P., McDermott J. Th e Long-Run Behavior of Commodity Prices: Small Trends and Big Variability. IMF Working Paper. 2001. May. URL:

https://www.imf.org/external/pubs/ft/wp/2001/wp0168.pdf

|

| [24] |

UN Data Shows That Ethanol is Not Causing Food Price Rises. The Global Renewable Fuels Alliance (GRFA). 2015. URL:

https://www.globalrfa.org/global-renewable-fuels-alliance-24/

|

| [25] |

Food Prices Dictated by Oil, Not Biofuel. Growty energy. 2022. March 15. URL:

https://growthenergy.org/2022/03/15/food-prices-dictated-by-oil-not-biofuel/

|

| [26] |

World Food and Oil Price Correlation. DeepResource. 2012. Аpr 26. URL:

https://deepresource.wordpress.com/2012/04/26/world-food-and-oil-price-correlation/

|

| [27] |

IGC. URL:

https://www.igc.int/en/default.aspx

|

| [28] |

Worldwide production of grain in 2022/23, by type. Statista. 2023. Feb 16. URL:

https://www.statista.com/statistics/263977/world-grain-production-by-type/

|

| [29] |

Lysenko O. The US recognized the risk of undermining the dominance of the dollar: what is really happening. Minfin. 2023. 26 квіт. URL:

https://minfin.com.ua/ua/currency/articles/ministr-finansov-ssha-priznala-risk-podryva-gospodstva-dollara-chto-proishodit-na-samom-dele/

[in Ukrainian].

|

Cite This Article

-

-

@article{10.11648/j.eco.20251402.11,

author = {Volodymyr Ognevyi},

title = {Reform of the Global Monetary System Supranational Currency GES

},

journal = {Economics},

volume = {14},

number = {2},

pages = {22-33},

doi = {10.11648/j.eco.20251402.11},

url = {https://doi.org/10.11648/j.eco.20251402.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.eco.20251402.11},

abstract = {The current crisis of the global monetary system forces the world community to search for ways of its reform. The focus is, first of all, on the issue of a qualitatively new international currency. In the context of this problem, a project is presented for the reincarnation of the Keynesian idea of an "objective standard of the value of a composite commodity", which in this case is the combined grain of the International Grains Council (IGC), with the aim of creating on its basis a supranational monetary unit GES (Grain Equivalent Standard) as an exchange rate benchmark /measure of value/ of national currencies plus for practical use as an international payment and reserve instrument. Since the movement of the market value of IGC grain is in the trend of the long-term movement of the value of the prevailing mass of commodity products, the new monetary architecture assumes, in essence, the binding of the GES currency to the general price trend of the world economy, which guarantees the stability of this currency in terms of purchasing power in the long term. – Guarantee of stability of global finances. Two options for reforming the global monetary system are proposed. The first option involves the creation of a global currency GES based on the weighted average value (in US dollars) on the world market of the IGC grain standard. – A symbolic currency, devoid of its own monetary base, is used as a measure of value and an international unit of account, an analogue of the SDR. The second option involves the creation of a global GES currency on its own monetary base, value-formatted by the global economy and attached to the weight of the IGC grain standard similar to the gold-dollar standard. – The currency is quite real, autonomous (independent of national currencies), used as a measure of value, a full-fledged means of monetary circulation, with the exception of bank lending. The first option involves linking the world currency to the market value of the IGC grain standard, the second – its direct value link to the weight of the IGC standard. Reforming the monetary system is designed to "anchor" national currencies (including the US dollar) on a solid material-value basis of the global economy, calm the emission-monetary bacchanalia in the world, stabilize the system of international settlements and payments, normalize equivalent commodity exchange in world trade, clearing pricing from pseudo-value falsity.

},

year = {2025}

}

Copy

|

Copy

|

Download

Download

-

TY - JOUR

T1 - Reform of the Global Monetary System Supranational Currency GES

AU - Volodymyr Ognevyi

Y1 - 2025/04/14

PY - 2025

N1 - https://doi.org/10.11648/j.eco.20251402.11

DO - 10.11648/j.eco.20251402.11

T2 - Economics

JF - Economics

JO - Economics

SP - 22

EP - 33

PB - Science Publishing Group

SN - 2376-6603

UR - https://doi.org/10.11648/j.eco.20251402.11

AB - The current crisis of the global monetary system forces the world community to search for ways of its reform. The focus is, first of all, on the issue of a qualitatively new international currency. In the context of this problem, a project is presented for the reincarnation of the Keynesian idea of an "objective standard of the value of a composite commodity", which in this case is the combined grain of the International Grains Council (IGC), with the aim of creating on its basis a supranational monetary unit GES (Grain Equivalent Standard) as an exchange rate benchmark /measure of value/ of national currencies plus for practical use as an international payment and reserve instrument. Since the movement of the market value of IGC grain is in the trend of the long-term movement of the value of the prevailing mass of commodity products, the new monetary architecture assumes, in essence, the binding of the GES currency to the general price trend of the world economy, which guarantees the stability of this currency in terms of purchasing power in the long term. – Guarantee of stability of global finances. Two options for reforming the global monetary system are proposed. The first option involves the creation of a global currency GES based on the weighted average value (in US dollars) on the world market of the IGC grain standard. – A symbolic currency, devoid of its own monetary base, is used as a measure of value and an international unit of account, an analogue of the SDR. The second option involves the creation of a global GES currency on its own monetary base, value-formatted by the global economy and attached to the weight of the IGC grain standard similar to the gold-dollar standard. – The currency is quite real, autonomous (independent of national currencies), used as a measure of value, a full-fledged means of monetary circulation, with the exception of bank lending. The first option involves linking the world currency to the market value of the IGC grain standard, the second – its direct value link to the weight of the IGC standard. Reforming the monetary system is designed to "anchor" national currencies (including the US dollar) on a solid material-value basis of the global economy, calm the emission-monetary bacchanalia in the world, stabilize the system of international settlements and payments, normalize equivalent commodity exchange in world trade, clearing pricing from pseudo-value falsity.

VL - 14

IS - 2

ER -

Copy

|

Download