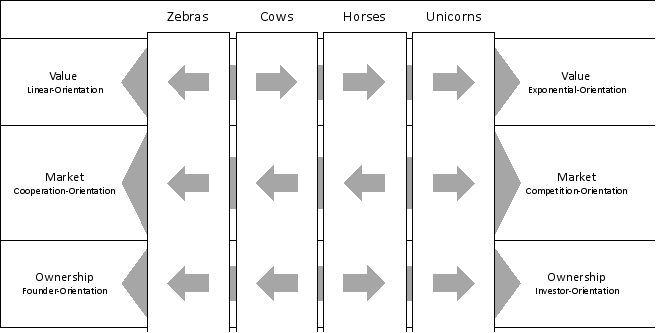

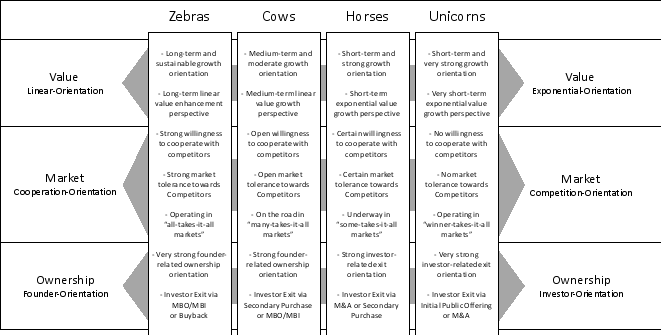

The development of a startup is determined by the entrepreneurial actions of its founders, and the associated entrepreneurial action theory accordingly describes the different goals, strategies, and measures of the founders for this development. The founders’ ambitions, which are a driving force behind entrepreneurial action, play a significant role in this context. Research shows that these ambitions determine the goals, strategies, and measures of the young company and, thus, the desired development from the founders’ perspective with the associated success. However, not every founder pursues the same ambitions in terms of content and form or always strives for the maximum. Based on three consecutive surveys (n = 1,985 startups), we use K-means cluster analysis to analyze three different dimensions of entrepreneurial ambition (growth, ownership, and cooperation) to examine their combined configuration. Based on this, we identified and double-checked four ambition groups with K-means cluster analysis and laid a foundation for a typology of startups based on the goals of their founders. The results have theoretical and practical implications for the founding and development of startups and a related focus on the founders’ ambitions, but also an associated broader consideration by potential investors.

| Published in | International Journal of Business and Economics Research (Volume 14, Issue 2) |

| DOI | 10.11648/j.ijber.20251402.11 |

| Page(s) | 38-55 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Startups, Founders, Ambitions, Typology, Characteristic, Classification

year |

| 2020 | 2021 | 2022 |

|---|---|---|---|---|

final sample |

| 761 | 671 | 553 |

startup age in years | 2.4 | 2.6 | 2.8 | |

2.04 | 2.04 | 2.3 | ||

0 | 0 | 0 | ||

9.92 | 9.33 | 9.83 | ||

number of founders | 1,910 | 1,750 | 1,372 | |

2.51 | 2.61 | 2.48 | ||

1.12 | 1.17 | 1.15 | ||

1 | 1 | 1 | ||

7 | 10 | 1,450 | ||

number of current employees | 9,526 | 8,639 | 12,436 | |

13.25 | 13.31 | 23.24 | ||

36.27 | 34.4 | 102.4 | ||

0 | 0 | 0 | ||

480 | 450 | 1,450 |

cluster | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

long-term linear vs. short-term exponential increase in value | -1.71 | 1.11 | 1.5 | 1.94 |

ownership vs. exit | -2.15 | -1.91 | 1.76 | 1.95 |

cooperation vs. competition | -1.23 | -1.22 | -1.63 | 1.1 |

ANOVA | ||||||

|---|---|---|---|---|---|---|

measure | cluster | error | ||||

mean of the squares | df | mean of the squares | df | F | Sig. | |

long-term linear vs. short-term exponential increase in value | 481.822 | 3 | .485 | 757 | 992.776 | .000 |

ownership vs. exit | 947.446 | 3 | .606 | 757 | 1563.266 | .000 |

cooperation vs. competition | 344.433 | 3 | .516 | 757 | 668.038 | .000 |

Zebra | Cow | Horse | Unicorn | ||

|---|---|---|---|---|---|

startup age in years |

| 2.34 | 2.14 | 2.4 | 2.61 |

| 1.98 | 2.04 | 1.93 | 2.14 | |

| 0 | 0 | 0 | 0 | |

| 8.33 | 9.92 | 9.08 | 9.83 | |

number of current employees |

| 5.76 | 5.5 | 15.71 | 21.17 |

| 14.28 | 8.09 | 38.61 | 50.64 | |

| 0 | 0 | 0 | 0 | |

| 130 | 52 | 350 | 480 |

SME | Small and Mid-sized Enterprise |

IPO | Initial Public Offering |

MBO | Management Buy-Out |

MBI | Management Buy-In |

M&A | Mergers and Acquisitions |

ANOVA | Analysis of Variance |

SPSS | Statistical Package for the Social Sciences |

EU | European Union |

| [1] | Angus, R. W., Packard, M. D., & Clark, B. B. (2023). Distinguishing unpredictability from uncertainty in entrepreneurial action theory. Small Business Economics, 60(3), 1147–1169. h |

| [2] | McMullen, J. S., & Dimov, D. (2013). Time and the entrepreneurial journey: The problems and promise of studying entrepreneurship as a process. Journal of Management Studies, 50(8), 1481–1512. |

| [3] | McMullen, J. S., & Shepherd, D. A. (2006). Entrepreneurial action and the role of uncertainty in the theory of the entrepreneur. Academy of Management Review, 31(1), 132–152. |

| [4] | Wood, M. S., Bakker, R. M., & Fisher, G. (2021). Back to the future: A time-calibrated theory of entrepreneurial action. Academy of Management Review, 46(1), 147–171. |

| [5] | Herbert, R. F., & Link, A. N. (1988). The entrepreneur: Mainstream views & radical critiques (2nd ed.). Praeger. |

| [6] | Schumpeter, J. A. (1934). The theory of economic development. MA: Harvard University Press. |

| [7] | Alvarez, S. A., & Parker, S. C. (2009). Emerging firms and the allocation of control rights: A Bayesian approach. The Academy of Management Review, 34(2), 209–227. |

| [8] | Davidsson, P. (2015). Entrepreneurial opportunities and the entrepreneurship nexus: A reconceptualization. Journal of Business Venturing, 30(5), 674–695. |

| [9] | Brown, L., Packard, M., & Bylund, P. (2018). Judgment, fast and slow: Toward a judgment view of entrepreneurs’ impulsivity. Journal of Business Venturing Insights, 10, 1–6. |

| [10] | Hunt, R. A., Lerner, D. A., Johnson, S. L., Badal, S., & Freeman, M. A. (2022). Cracks in the wall: Entrepreneurial action theory and the weakening presumption of intended rationality. Journal of Business Venturing, 37(3), 1–22. |

| [11] | Dimov, D. (2010). Nascent entrepreneurs and venture emergence: Opportunity confidence, human capital, and early planning. Journal of Management Studies, 47(6), 1123–1153. |

| [12] | Sarasvathy, S. D. (2001). Causation and effectuation: Toward a theoretical shift from economic inevitability to entrepreneurial contingency. The Academy of Management Review, 26(2), 243–263. |

| [13] | Nelson, T. (2003). The persistence of founder influence: Management, ownership, and performance effects at initial public offering. Strategic Management Journal, 24(8), 707–724. |

| [14] | Robbins, S. P., & Judge, T. A. (2013). Organizational Behavoir (15th ed.). Pearson Education Limited. |

| [15] | Hannah, D. P., & Eisenhardt, K. M. (2018). How firms navigate cooperation and competition in nascent ecosystems. Strategic Management Journal, 39(12), 3163–3192. |

| [16] | Stephan, U., Hart, M., Mickiewicz, T., & Drews, C.-C. (2015). Understanding motivations for entrepreneurship (Issue 212). |

| [17] | Judge, T. A., & Kammeyer-Mueller, J. D. (2012). On the Value of Aiming High: The Causes and Consequences of Ambition. Journal of Applied Psychology, 97(4), 758–775. |

| [18] | Shane, S., Locke, E. A., & Collins, C. J. (2003). Entrepreneurial motivation. Human Resource Management Review, 13, 257–279. |

| [19] | Sims, R. L., & Chinta, R. (2020). The mediating role of entrepreneurial ambition in the relationship between entrepreneurial efficacy and entrepreneurial drive for female nascent entrepreneurs. Gender in Management: An International Journal, 35(1), 76–91. |

| [20] | Hermans, J., Vanderstraeten, J., van Witteloostuijn, A., Dejardin, M., Ramdani, D., & Stam, E. (2015). Ambitious entrepreneurship: A review of growth aspirations, intentions, and expectations. In A. C. Corbett, J. A. Katz, & A. Mckelvie (Eds.), Advances in Entrepreneurship, Firm Emergence and Growth (Vol. 17, pp. 127–160). Emerald Group Publishing Limited. |

| [21] | Stam, E., Hartog, C., Stel, A. van, & Thurik, R. (2011). Ambitious entrepreneurship, high-growth firms, and macroeconomic growth. In M. Minniti (Ed.), The Dynamics of Entrepreneurship: Evidence from global entrepreneurship monitor data (1st ed., pp. 231–250). Oxford University Press. |

| [22] | Kleinert, S. (2023). The promise of new ventures’ growth ambitions in early-stage funding: On the crossroads between cheap talk and credible signals. Entrepreneurship: Theory and Practice, 48(1), 1–36. |

| [23] | Verheul, I., & Van Mil, L. (2011). What determines the growth ambition of Dutch early-stage entrepreneurs? International Journal of Entrepreneurial Venturing, 3(2), 183–207. |

| [24] | Kirkley, W. W. (2016). Entrepreneurial behaviour: The role of values. International Journal of Entrepreneurial Behaviour and Research, 22(3), 290–328. |

| [25] | Frese, M., & Gielnik, M. M. (2014). The Psychology of Entrepreneurship. Annual Review of Organizational Psychology and Organizational Behavior, 1, 413–438. |

| [26] | Kirkpatrick, S. A., & Locke, E. A. (1996). Direct and indirect effects of three core charismatic leadership components on performance and attitudes. Journal of Applied Psychology, 81(1), 36–51. |

| [27] | Locke, E. A., & Latham, G. P. (2002). Building a practically useful theory of goal setting and task motivation: A 35-year odyssey. American Psychologist, 57(9), 705–717. |

| [28] | Dutta, D. K., & Thornhill, S. (2008). The evolution of growth intentions: Toward a cognition-based model. Journal of Business Venturing, 23(3), 307–332. |

| [29] | Kolvereid, L. (1992). Growth aspirations among Norwegian entrepreneurs. Journal of Business Venturing, 7(3), 209–222. |

| [30] | Lecuna, A. (2024). Understanding imagination in entrepreneurship. Entrepreneurship Research Journal, 14(2), 373–400. |

| [31] | Newman, A., Obschonka, M., Moeller, J., & Chandan, G. G. (2021). Entrepreneurial passion: A review, synthesis, and agenda for future research. Applied Psychology, 70(2), 816–860. |

| [32] | Hambrick, D. C. (2007). Upper echelons theory: An update. Academy of Management Review, 32(2), 334–343. |

| [33] | Hambrick, D. C., & Mason, P. A. (1984). Upper echelons: The organization as a reflection of its top managers. Academy of Management Review, 9(2), 193–206. |

| [34] | Bosma, N., & Schutjens, V. (2009). Determinants of early-stage entrepreneurial activity in European regions: distinguishing low and high ambition entrepreneurship. In D. Smallbone, H. Landström, & D. Jones-Evans (Eds.), Entrepreneurship and Growth in Local, Regional and National Economies: Frontiers in European Entrepreneurship Research, 49–77. |

| [35] | Cassar, G. (2007). Money, money, money? A longitudinal investigation of entrepreneur career reasons, growth preferences and achieved growth. Entrepreneurship & Regional Development, 19(1), 89–107. |

| [36] | Kuckertz, A., Scheu, M., & Davidsson, P. (2023). Chasing mythical creatures – A (not-so-sympathetic) critique of entrepreneurship’s obsession with unicorn startups. Journal of Business Venturing Insights, 19. |

| [37] | Collewaert, V. (2012). Angel investors’ and entrepreneurs’ intentions to exit their ventures: A conflict perspective. Entrepreneurship Theory and Practice, 36(4), 753–779. |

| [38] | Gundry, L. K., & Welsch, H. P. (2001). The ambitious entrepreneur: High growth strategies of women-owned enterprises. Journal of Business Venturing, 16(5), 453–470. |

| [39] | Galloway, L., & Mochrie, R. (2006). Entrepreneurial motivation, orientation and realization in rural economies. The International Journal of Entrepreneurship and Innovation, 7(3), 173–183. |

| [40] | Wennberg, K., Wiklund, J., DeTienne, D. R., & Cardon, M. S. (2010). Reconceptualizing entrepreneurial exit: Divergent exit routes and their drivers. Journal of Business Venturing, 25(4), 361–375. |

| [41] | Kung, F. Y. H., & Scholer, A. A. (2020). The pursuit of multiple goals. Social and Personality Psychology Compass, 14(1), 1–14. |

| [42] | Smith, K. G., Locke, E. A., & Barry, D. (1990). Goal setting, planning, and organizational performance: An experimental simulation. Organizational Behavior and Human Decision Processes, 46(1), 118–134. |

| [43] | Arabiun, A., Salajegheh, N., Aeeni, Z., & Forghani, A. K. (2023). Trends and patterns in entrepreneurial action research: A bibliometric overview and research agenda. Journal of Global Entrepreneurship Research, 13(8). |

| [44] | Aldrich, H. E., & Ruef, M. (2018). Unicorns, gazelles, and other distractions on the way to understanding real entrepreneurship in the United States. Academy of Management Perspectives, 32(4), 458–472. |

| [45] | Morris, M. H., & Kuratko, D. F. (2020). What do entrepreneurs create? Understanding different venture types. Edward Elgar Press. |

| [46] | Kuratko, D. F., & Audretsch, D. B. (2022). The future of entrepreneurship: The few or the many? Small Business Economics, 59(1), 269–278. |

| [47] |

Chan, A. (2019), The full taxonomy of startups: We talk about Unicorns, but there’s also Dragons, Pegasus, and even Ponies.

https://medium.com/swlh/the-full-taxonomy-forstartups-2e10d56f8238 |

| [48] |

Rice, M. (2020). What animal is your startup? Zebras, Camels, Gazelles, oh my!

https://builtin.com/growth-hacking/startup-animals-zebras-camels-gazelles |

| [49] | Brandel, J., Zepeda, M., Scholz, A., & Williams, A. (2017). Zebras fix what unicorns break. Medium. |

| [50] |

Shaw, J. (2017). Unicorns vs. Zebras: What type of entrepreneur are you? Small Business Forum.

https://smallbusinessforum.co/unicorns-vs-zebras-what-type-of-entrepreneur-are-you-2636424193ed |

| [51] | Shane, S. (2003). A general theory of entrepreneurship: The individual-opportunity nexus. Edward Elgar. |

| [52] | Alvarez, S. A., & Barney, J. B. (2007). Discovery and creation: Alternative theories of entrepreneurial action. Strategic Entrepreneurship Journal, 1(1–2), 11–26. |

| [53] | Elchardus, M., & Smits, W. (2008). The vanishing flexible: Ambition, self-realization and flexibility in the career perspectives of young Belgian adults. Work, Employment and Society, 22(2), 243–262. |

| [54] | Desrochers, S., & Dahir, V. (2000). Ambition as a motivational basis of organizational and professional commitment: Preliminary analysis of a proposed career advancement ambition scale. Perceptual and Motor Skills, 91(2), 563–570. |

| [55] | Krishnamoorthy, V., & Balasubramani, R. (2014). Motivational factors among women entrepreneurs and their entrepreneurial success: A study. International Journal of Management Research and Business Strategy, 3(2), 12–26. |

| [56] | Stam, E., Bosma, N., Van Witteloostuijn, A., De Jong, J. P. J., Bogaert, S., Edwards, N., & Jaspers, F. (2012). Ambitious entrepreneurship: A review of the academic literature and new directions for public policy. In Report for the Advisory Council for Science and Technology Policy (AWT) and the Flemish Council for Science and Innovation (VRWI). |

| [57] | Wallin, A., Still, K., & Henttonen, K. (2016). Entrepreneurial growth ambitions: The case of Finish technology startups. Technology Innovation Management Review, 6(10), 5–16. |

| [58] | Estrin, S., Mickiewicz, T., & Rebmann, A. (2017). Prospect theory and the effects of bankruptcy laws on entrepreneurial aspirations. Small Business Economics, 48(4), 977–997. |

| [59] | Hmieleski, K. M., & Baron, R. A. (2009). Entrepreneurs’ optimism and new venture performance: A social cognitive perspective. Academy of Management Journal, 52(3), 473–488. |

| [60] | Johnson, S. L., Madole, J. W., & Freeman, M. A. (2018). Mania risk and entrepreneurship: Overlapping personality traits. Academy of Management Perspectives, 32(2), 207–227. |

| [61] | Sapienza, H. J., Korsgaard, M. A., & Forbes, D. P. (2003). The self-determination motive and entrepreneurs’ choice of financing. In J. A. Katz & D. A. Shepherd (Eds.), Cognitive Approaches to Entrepreneurship Research (Advances in entrepreneurship, firm emergence, and growth) (Vol. 6, pp. 105–138). Emerald Group Publishing Limited. |

| [62] | Guzmán, J., & Santos, F. J. (2001). The booster function and the entrepreneurial quality: An application to the province of Seville. Entrepreneurship and Regional Development, 13, 211–228. |

| [63] | Kirchhoff, B. A. (1994). Entrepreneurship and dynamic capitalism: The economics of business firm formation and growth. |

| [64] | Mangematin, V., Lemarié, S., Boissin, J.-P., Catherine, D., Corolleur, F., Coronini, R., & Trommetter, M. (2003). Development of SMEs and heterogeneity of trajectories: The case of biotechnology in France. Research Policy, 32(4), 621–638. |

| [65] | Bengtsson, M., & Kock, S. (1999). Cooperation and competition in relationships between competitors in business networks. Journal of Business & Industrial Marketing, 14(3), 178–194. |

| [66] | Novari, E. (2020). The SMEs performance: Mediation of ambitious entrepreneur. International Journal of Psychosocial Rehabilitation, 24(8), 4828–4839. |

| [67] | Ali, A., Espinosa, J. E. A., Hart, M., Kelley, D., Levie, J., Morris, R., Drexler, M., Eltobgy, M., & Gratzke, P. (2015). Leveraging entrepreneurial ambition and innovation: A global perspective on entrepreneurship, competitiveness and development. |

| [68] | Stam, E., & Wennberg, K. (2009). The roles of R&D in new firm growth. Small Business Economics, 33(1), 77–89. |

| [69] | Culkin, N., & Smith, D. (2000). An emotional business: A guide to understanding the motivations of small business decision takers. Qualitative Market Research: An International Journal, 3(3), 145–157. |

| [70] | Bosma, N., & Schutjens, V. (2007). Patterns of promising entrepreneurial activity in European regions. Tijdschrift Voor Economische En Sociale Geografie, 98(5), 675–686. |

| [71] | Malsch, F., & Guieu, G. (2019). How to get more with less? Scarce resources and high social ambition: effectuation as KM tool in social entrepreneurial projects. Journal of Knowledge Management, 23(10), 1949–1964. |

| [72] | Foucrier, T., & Wiek, A. (2019). A process-oriented framework of competencies for sustainability entrepreneurship. Sustainability (Switzerland), 11(24), 7250–7268. h |

| [73] | DeTienne, D. R., McKelvie, A., & Chandler, G. N. (2015). Making sense of entrepreneurial exit strategies: A typology and test. Journal of Business Venturing, 30(2), 255–272. |

| [74] | Block, J. H., Kohn, K., Miller, D., & Ullrich, K. (2015). Necessity entrepreneurship and competitive strategy. Small Business Economics, 44(1), 37–54. |

| [75] | Kollmann, T., Stöckmann, C., Niemand, T., Hensellek, S., & de Cruppe, K. (2021). A configurational approach to entrepreneurial orientation and cooperation explaining product/service innovation in digital vs. non-digital startups. Journal of Business Research, 125(March 2021), 508–519. |

| [76] | Bhardwaj, G., Camillus, J. C., & Hounshell, D. A. (2006). Continual corporate entrepreneurial search for long-term growth. Management Science, 52(2), 248–261. |

| [77] | Davidsson, P. (1989). Entrepreneurship — And after? A study of growth willingness in small firms. Journal of Business Venturing, 4(3), 211–226. |

| [78] | Markman, G. D., & Gartner, W. B. (2002). Is Extraordinary Growth Profitable? A Study of Inc. 500 High-Growth Companies. Entrepreneurship Theory and Practice, 27(1), 65–75. |

| [79] | Carr, Jon. C., Haggard, K. S., Hmieleski, K. M., & Zahra, S. A. (2010). A study of the moderating effects of firm age at internationalization on firm survival and short-term growth. Strategic Entrepreneurship Journal, 4(2), 183–192. |

| [80] | Cavallo, A., Cosenz, F., & Noto, G. (2023). Business model scaling and growth hacking in digital entrepreneurship. Journal of Small Business Management, 00(00), 1–28. |

| [81] | Darnihamedani, P., & Terjesen, S. (2020). Male and female entrepreneurs’ employment growth ambitions: The contingent role of regulatory efficiency. Small Business Economics, 58(1), 185–204. |

| [82] | Ginn, C. W., & Sexton, D. L. (1990). A comparison of the personality type dimensions of the 1987 Inc. 500 company founders/CEOs with those of slower-growth firms. Journal of Business Venturing, 5(5), 313–326. |

| [83] | Sedláček, P., & Sterk, V. (2017). The growth potential of startups over the business cycle. American Economic Review, 107(10), 3182–3210. |

| [84] | Sterk, V., Sedláček, P., & Pugsley, B. (2021). The nature of firm growth. American Economic Review, 111(2), 547–579. |

| [85] | Wennberg, K., Delmar, F., & McKelvie, A. (2016). Variable risk preferences in new firm growth and survival. Journal of Business Venturing, 31(4), 408–427. |

| [86] | Yim, H. R. (2008). Quality shock vs. market shock: Lessons from recently established rapidly growing U.S. Startups. Journal of Business Venturing, 23(2), 141–164. |

| [87] | Henrekson, M., & Stenkula, M. (2010). Entrepreneurship and public policy. In Handbook of Entrepreneurship Research (pp. 595–637). |

| [88] | Stam, E. (2015). Entrepreneurial ecosystems and regional policy: A sympathetic critique. European Planning Studies, 23(9), 1759–1769. |

| [89] | Davis, J. H., Schoorman, F. D., & Donaldson, L. (1997). Toward a stewardship theory of management. The Academy of Management Review, 22(1), 20–47. |

| [90] | Dawson, A., Paeglis, I., & Basu, N. (2018). Founder as steward or agent? A study of founder ownership and firm value. Entrepreneurship Theory and Practice, 42(6), 886–910. |

| [91] | Burkart, M., Panunzi, F., & Shleifer, A. (2003). Family firms. The Journal of Finance, 58(5), 2167–2201. |

| [92] | Villalonga, B., & Amit, R. (2020). Family ownership. Oxford Review of Economic Policy, 36(2), 241–257. |

| [93] | Gimeno, J., Folta, T. B., Cooper, A. C., & Woo, C. Y. (1997). Survival of the fittest? Entrepreneurial human capital and the persistence of underperforming firms. Administrative Science Quarterly, 42(4), 750–783. |

| [94] | Youne, J., & Jeon, B. (2024). The Effects of Positive Psychological Capital on Innovative Behavior and Turnover Intention of the Start-ups employees: Focused on the Moderating Effects of Gender and Job Position. The Korean Career, Entrepreneurship & Business Association. |

| [95] | DeTienne, D. R., Shepherd, D. A., & De Castro, J. O. (2008). The fallacy of “only the strong survive”: The effects of extrinsic motivation on the persistence decisions for underperforming firms. Journal of Business Venturing, 23(5), 528–546. |

| [96] | Shepherd, D. A., Williams, T. A., & Patzelt, H. (2015). Thinking about entrepreneurial decision making: Review and research agenda. Journal of Management, 41(1), 11–46. |

| [97] | Hong, S., Serfes, K., & Thiele, V. (2020). Competition in the venture capital market and the success of startup companies: Theory and evidence. Journal of Economics & Management Strategy, 29(4), 741–791. |

| [98] | DeTienne, D. R. (2010). Entrepreneurial exit as a critical component of the entrepreneurial process: Theoretical development. Journal of Business Venturing, 25(2), 203–215. |

| [99] | Lindblom, A., Lindblom, T., & Wechtler, H. (2020). Dispositional optimism, entrepreneurial success and exit intentions: The mediating effects of life satisfaction. Journal of Business Research, 120, 230–240. |

| [100] | Jain, B. A., & Kini, O. (1999). The life cycle of initial public offering firms. Journal of Business Finance & Accounting, 26(9), 1281–1307. |

| [101] | Scholes, L., Westhead, P., & Burrows, A. (2008). Family firm succession: The management buy-out and buy-in routes. Journal of Small Business and Enterprise Development, 15(1), 8–30. |

| [102] | Coyle, B. (2000). Mergers and Acquisitions. Glenlake Publishing Company, Fitzroy Dearborn Publishers. |

| [103] | Teece, D. J. (1992). Competition, cooperation, and innovation: Organizational arrangements for regimes of rapid technological progress. Journal of Economic Behavior & Organization, 18(1), 1–25. |

| [104] | Østbye, S. E., & Roelofs, M. R. (2012). The competition–innovation debate: is R&D cooperation the answer? Economics of Innovation and New Technology, 22(2), 153–176. |

| [105] | Benavides Espinosa, M. D. M., & Mohedano Suanes, A. (2011). Corporate entrepreneurship through joint venture. International Entrepreneurship and Management Journal, 7(3), 413–430. |

| [106] | Rezazadeh, A., & Nobari, N. (2018). Antecedents and consequences of cooperative entrepreneurship: a conceptual model and empirical investigation. International Entrepreneurship and Management Journal, 14(2), 479–507. |

| [107] | Ford, D., & Håkansson, H. (2013). Competition in business networks. Industrial Marketing Management, 42(7), 1017–1024. |

| [108] | Ergun, O., Kuyzu, G., & Savelsbergh, M. (2007). Reducing truckload transportation costs through collaboration. Transportation Science, 41(2), 206–221. |

| [109] | Friday, D., Ryan, S., Sridharan, R., & Collins, D. (2018). Collaborative risk management: a systematic literature review. International Journal of Physical Distribution and Logistics Management, 48(3), 231–253. |

| [110] | Ahuja, G. (2000). Collaboration networks, structural holes, and innovation: A longitudinal study. Administrative Science Quarterly, 45(3), 425–455. |

| [111] | Sytch, M., & Tatarynowicz, A. (2014). Friends and foes: The dynamics of dual social structures. Academy of Management Journal, 57(2), 585–613. |

| [112] | Dew, N., Read, S., Sarasvathy, S. D., & Wiltbank, R. (2009). Effectual versus predictive logics in entrepreneurial decision-making: Differences between experts and novices. Journal of Business Venturing, 24(4), 287–309. |

| [113] | Dowling, M., & Helm, R. (2006). Product development success through cooperation: A study of entrepreneurial firms. Technovation, 26(4), 483–488. |

| [114] | Hoffmann, W., Lavie, D., Reuer, J. J., & Shipilov, A. (2018). The interplay of competition and cooperation. Strategic Management Journal, 39, 3033–3052. |

| [115] | Jacobides, M. G., MacDuffie, J. P., & Tae, C. J. (2016). Agency, structure, and the dominance of OEMs: Change and stability in the automotive sector. Strategic Management Journal, 37(9), 1942–1967. |

| [116] | Freeman, J., & Engel, J. S. (2007). Models of Innovation: Startups and Mature Corporations. California Management Review, 50(1), 94–119. |

| [117] |

Hayes, A. (2022). Winner-Takes-All Market: Definition, examples, economic impact. Investopedia.

https://www.investopedia.com/terms/w/winner-takes-all-market.asp |

| [118] | Lebo, M. J., & Weber, C. (2015). An effective approach to the repeated cross-sectional design. American Journal of Political Science, 59(1), 242–258. |

| [119] |

Kollmann, T., Kleine-Stegemann, L., Then-Bergh, C., Harr, M. D., Hirschfeld, A., Gilde, J., & Walk, V. (2021). German Startup Monitor 2021.

https://deutschestartups.org/wp-content/uploads/2021/10/Deutscher-Startup-Monitor_2021.pdf |

| [120] | Liedtke, M., Asghari, R., & Spengler, T. (2021). Fostering entrepreneurial ecosystems and the choice of location for new companies in rural areas – the case of Germany. Journal of Small Business Strategy, 31(4), 76–87. |

| [121] | Carland, J. W., Hoy, F., Boulton, W. R., & Carland, J. A. C. (1984). Differentiating entrepreneurs from small business owners: A conceptualization. Academy of Management Review, 9(2), 354–359. |

| [122] | Kollmann, T., Jung, P. B., Kleine-Stegemann, L., Ataee, J., & de Cruppe, K. (2020). German Startup Monitor 2020. |

| [123] |

Kollmann, T., Strauß, C., Pröpper, A., Faasen, C., Hirschfeld, A., Gilde, J., & Walk, V. (2022). German Startup Monitor 2022.

https://startupverband.de/fileadmin/startupverband/mediaarchiv/research/dsm/DSM_2022.pdf |

| [124] | Diamantopoulos, A., Sarstedt, M., Fuchs, C., Wilczynski, P., & Kaiser, S. (2012). Guidelines for choosing between multi-item and single-item scales for construct measurement: A predictive validity perspective. Journal of the Academy of Marketing Science, 40(3), 434–449. |

| [125] | Bergkvist, L., & Rossiter, J. R. (2007). The predictive validity of multiple-item versus single-item measures of the same constructs. Journal of Marketing Research, 44(2), 175–184. |

| [126] | Matthews, R. A., Pineault, L., & Hong, Y.-H. (2022). Normalizing the use of single-item measures: Validation of the single-item compendium for organizational psychology. Journal of Business and Psychology, 37, 639–673. |

| [127] | Drolet, A. L., & Morrison, D. G. (2001). Do we really need multiple-item measures in service research? Journal of Service Research, 3(3), 196–204. |

| [128] | Rogelberg, S. G., & Stanton, J. M. (2007). Introduction: Understanding and dealing with organizational survey nonresponse. Organizational Research Methods, 10(2), 195–209. |

| [129] | Fisher, G. G., Matthews, R. A., & Gibbons, A. M. (2016). Developing and investigating the use of single-item measures in organizational research. Journal of Occupational Health Psychology, 21(1), 3–23. |

| [130] | Friborg, O., Martinussen, M., & Rosenvinge, J. H. (2006). Likert-based vs. semantic differential-based scorings of positive psychological constructs: A psychometric comparison of two versions of a scale measuring resilience. Personality and Individual Differences, 40(5), 873–884. |

| [131] | Brettel, M., Mauer, R., Engelen, A., & Küpper, D. (2012). Corporate effectuation: Entrepreneurial action and its impact on R&D project performance. Journal of Business Venturing, 27(2), 167–184. |

| [132] | Blasius, J., & Thiessen, V. (2001). The Use of Neutral Responses in Survey Questions: An Application of Multiple Correspondence Analysis. Journal of Official Statistics, 17(3), 351–367. |

| [133] | Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2019). Multivariate data analysis (8th ed.). Cengage. |

| [134] | Hartigan, J. A. (1975). Clustering algorithms. In Wiley (1st ed.). John Wiley & Sons. |

| [135] | Hartigan, J. A., & Wong, M. A. (1979). Algorithm AS 136: A K-means clustering algorithm. Journal of the Royal Statistical Society. Series C (Applied Statistics), 28(1), 100–108. |

| [136] | Gibson, C. B., & Birkinshaw, J. (2004). The antecedents, consequences, and mediating role of organizational ambidexterity. Academy of Management Journal, 47(2), 209–226. |

| [137] | Hennig, C., & Liao, T. F. (2013). How to find an appropriate clustering for mixed-type variables with application to socio-economic stratification. Journal of the Royal Statistical Society: Series C (Applied Statistics), 62(3), 309–369. |

| [138] | Joshi, K. A. (2019). Specialisation and syndication as risk management strategies for venture capital firms in India. International Journal of Entrepreneurial Venturing, 11(6), 541–567. |

| [139] | Lubatkin, M. H., Simsek, Z., Ling, Y., & Veiga, J. F. (2006). Ambidexterity and performance in small- to medium-sized firms: The pivotal role of top management team behavioral integration. Journal of Management, 32(5), 646–672. |

| [140] | Chen, Y., & Tu, L. (2007). Density-based clustering for real-time stream data. Proceedings of the 13th ACM SIGKDD International Conference on Knowledge Discovery and Data Mining - KDD ’07, 133. |

| [141] | Olukanmi, P. O., & Twala, B. (2017). K-means-sharp: Modified centroid update for outlier-robust k-means clustering. 2017 Pattern Recognition Association of South Africa and Robotics and Mechatronics (PRASA-RobMech), 14–19. |

| [142] | Venâncio, A., Picoto, W., & Pinto, I. (2023). Time-to-unicorn and digital entrepreneurial ecosystems. Technological Forecasting and Social Change, 190. |

| [143] | Kollmann, T., & Kleine-Stegemann, L. (2021). The Startup-Zoo: A Typology for Founders and Investors. |

| [144] | Wright, M., Robbie, K., & Ennew, C. (1997). Venture capitalists and serial entrepreneurs. Journal of Business Venturing, 12(3), 227–249. |

| [145] |

Selby, J. (2020). Unicorn companies vs. zebra companies: Which is better? Foundershield.

https://foundershield.com/blog/unicorn-companies-vs-zebra-companies/ |

| [146] | Davidsson, P., & Honig, B. (2003). The role of social and human capital among nascent entrepreneurs. Journal of Business Venturing, 18(3), 301–331. |

| [147] | Powell, E. E., & Baker, T. (2017). In the beginning: Identity processes and organizing in multi-founder nascent ventures. Academy of Management Journal, 60(6), 2381–2414. |

| [148] | CB Insights. (2023). The Complete List Of Unicorn Companies. |

APA Style

Kollmann, T., Pröpper, A. (2025). The Startup-Zoo: A Typology of Startups Based on the Ambitions of Their Founders. International Journal of Business and Economics Research, 14(2), 38-55. https://doi.org/10.11648/j.ijber.20251402.11

ACS Style

Kollmann, T.; Pröpper, A. The Startup-Zoo: A Typology of Startups Based on the Ambitions of Their Founders. Int. J. Bus. Econ. Res. 2025, 14(2), 38-55. doi: 10.11648/j.ijber.20251402.11

@article{10.11648/j.ijber.20251402.11,

author = {Tobias Kollmann and Anna Pröpper},

title = {The Startup-Zoo: A Typology of Startups Based on the Ambitions of Their Founders

},

journal = {International Journal of Business and Economics Research},

volume = {14},

number = {2},

pages = {38-55},

doi = {10.11648/j.ijber.20251402.11},

url = {https://doi.org/10.11648/j.ijber.20251402.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijber.20251402.11},

abstract = {The development of a startup is determined by the entrepreneurial actions of its founders, and the associated entrepreneurial action theory accordingly describes the different goals, strategies, and measures of the founders for this development. The founders’ ambitions, which are a driving force behind entrepreneurial action, play a significant role in this context. Research shows that these ambitions determine the goals, strategies, and measures of the young company and, thus, the desired development from the founders’ perspective with the associated success. However, not every founder pursues the same ambitions in terms of content and form or always strives for the maximum. Based on three consecutive surveys (n = 1,985 startups), we use K-means cluster analysis to analyze three different dimensions of entrepreneurial ambition (growth, ownership, and cooperation) to examine their combined configuration. Based on this, we identified and double-checked four ambition groups with K-means cluster analysis and laid a foundation for a typology of startups based on the goals of their founders. The results have theoretical and practical implications for the founding and development of startups and a related focus on the founders’ ambitions, but also an associated broader consideration by potential investors.

},

year = {2025}

}

TY - JOUR T1 - The Startup-Zoo: A Typology of Startups Based on the Ambitions of Their Founders AU - Tobias Kollmann AU - Anna Pröpper Y1 - 2025/03/07 PY - 2025 N1 - https://doi.org/10.11648/j.ijber.20251402.11 DO - 10.11648/j.ijber.20251402.11 T2 - International Journal of Business and Economics Research JF - International Journal of Business and Economics Research JO - International Journal of Business and Economics Research SP - 38 EP - 55 PB - Science Publishing Group SN - 2328-756X UR - https://doi.org/10.11648/j.ijber.20251402.11 AB - The development of a startup is determined by the entrepreneurial actions of its founders, and the associated entrepreneurial action theory accordingly describes the different goals, strategies, and measures of the founders for this development. The founders’ ambitions, which are a driving force behind entrepreneurial action, play a significant role in this context. Research shows that these ambitions determine the goals, strategies, and measures of the young company and, thus, the desired development from the founders’ perspective with the associated success. However, not every founder pursues the same ambitions in terms of content and form or always strives for the maximum. Based on three consecutive surveys (n = 1,985 startups), we use K-means cluster analysis to analyze three different dimensions of entrepreneurial ambition (growth, ownership, and cooperation) to examine their combined configuration. Based on this, we identified and double-checked four ambition groups with K-means cluster analysis and laid a foundation for a typology of startups based on the goals of their founders. The results have theoretical and practical implications for the founding and development of startups and a related focus on the founders’ ambitions, but also an associated broader consideration by potential investors. VL - 14 IS - 2 ER -

Faculty of Computer Science, esp. Digital Business and Digital Entrepreneurship, University of Duisburg-Essen, Essen, Germany

Faculty of Computer Science, esp. Digital Business and Digital Entrepreneurship, University of Duisburg-Essen, Essen, Germany

Information