The primary motive of this paper was to investigate the impact of Foreign Direct Investment on economic growth of Nigeria from 1985 to 2022. Ex – post facto research design was carefully carried out; annual time series data were extracted from Central Bank of Nigeria Statistical Bulletin of 2021 and World Development Indicator. Real Gross Domestic Product (RGDP) was used as the dependent variable proxy for economic growth. Foreign Direct Investment (FDI), Exchange Rate (EXCR), Trade Openness (TOPN) and Inflation (INF) all denoted for explanatory variables of the study. The estimated coefficients of the variables under study displayed that all the variables are integrated of the same order 1(1) exception of Foreign Direct Investment which was integrated of order 1(0). The bound test conducted showed that there is proof of the presence of a long run correlation among the variables used while the causality test clearly showed that FDI granger causes economic growth in Nigeria under review. Other diagnostic tests seen in this paper are unit root test, descriptive statistics, correlation coefficient matrix, Cointegration test and test of Normality respectively, and they long-established the validity and reliability of the model used. Based on the inferential results revealed by the research work, the paper came up with recommendation that government should improve the investment climate for both domestic and foreign investors through adequate infrastructural development, soft loans and tax holidays.

| Published in | International Journal of Economic Behavior and Organization (Volume 12, Issue 2) |

| DOI | 10.11648/j.ijebo.20241202.11 |

| Page(s) | 46-66 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2024. Published by Science Publishing Group |

Economic Growth, Foreign Direct Investment, Inflation, Nigeria, ARDL

LNRGDP | FDI | LNTOPN | EXCR | INF | |

|---|---|---|---|---|---|

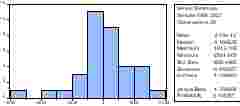

Mean | 26.23412 | 1.734142 | 4.131049 | 111.0959 | 17.80978 |

Median | 26.17273 | 1.552115 | 4.106532 | 120.5782 | 11.11892 |

Maximum | 26.94374 | 5.790847 | 4.591999 | 306.9210 | 75.40165 |

Minimum | 25.54105 | 0.195183 | 3.801428 | 4.016037 | 0.686099 |

Std. Dev. | 0.484815 | 1.253109 | 0.202225 | 91.13162 | 15.48021 |

Skewness | 0.197452 | 1.648725 | 0.656290 | 0.649534 | 1.916839 |

Kurtosis | 1.469190 | 5.591822 | 3.079082 | 2.747842 | 7.170330 |

Jarque-Bera | 3.436580 | 24.18725 | 2.377539 | 2.407848 | 44.12202 |

Probability | 0.179373 | 0.000006 | 0.304596 | 0.300015 | 0.000000 |

Sum | 865.7261 | 57.22670 | 136.3246 | 3666.164 | 587.7228 |

Sum Sq. Dev. | 7.521469 | 50.24900 | 1.308639 | 265759.1 | 7668.382 |

Observations | 38 | 38 | 38 | 38 | 38 |

At level | After first differencing | ||||||

|---|---|---|---|---|---|---|---|

Variables | ADF test statistic | Critical value at 10% | Remarks | ADF test statistics | Critical value at 10% | Remarks | Order of integration |

LNRGDP | -0.485998 | -2.957110 | NS | -3.399034 | -2.957110 | S | I(1) |

FDI | -3.812357 | -2.957110 | S | -7.245961 | -2.960411 | S | I(0) |

LNTOPN | -2.703001 | -2.954021 | NS | -7.088551 | -2.957110 | S | I(1) |

EXR | 1.643233 | -2.954021 | NS | -3.911390 | -2.957110 | S | I(1) |

INF | -2.932556 | -2.954021 | NS | -3.920520 | -2.963972 | S | I(1) |

Test Statistic | Value | Significance | I(0) | I(1) |

|---|---|---|---|---|

F-statistic | 8.487773 | 10% | 2.68 | 3.53 |

K | 4 | 5% | 3.05 | 3.97 |

1% | 3.81 | 4.92 |

Variable | Co-efficient | Std. Error | t-statistic | Prob |

|---|---|---|---|---|

D(FDI(-1)) | -0.049375 | 0.007362 | -6.707090 | 0.0001 |

D(LNTOPN(-1)) | 0.051979 | 0.023234 | 2.237205 | 0.0521 |

D(EXCR(-1)) | -0.000491 | 0.000208 | -2.358258 | 0.0427 |

D(INF(-1)) | 0.002894 | 0.000524 | 5.521703 | 0.0004 |

D(FDI) | 0.010150 | 0.003412 | 2.974469 | 0.0156 |

D(LNTOPN) | -0.018361 | 0.021641 | -0.848439 | 0.4182 |

D(EXCR) | -0.000464 | 0.000208 | -2.234572 | 0.0523 |

D(INF) | -0.000267 | 0.000344 | -0.776574 | 0.4573 |

C | 10.97189 | 1.227324 | 8.939684 | 0.0000 |

CointEq(-1)* | -0.419927 | 0.047180 | -8.900518 | 0.0000 |

R-squared | 0.899514 |

Adjusted R-squared | 0.799029 |

S. E. of regression | 0.016279 |

F-statistic | 8.951684 |

Prob(F-statistic) | 0.000102 |

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

|---|---|---|---|---|

FDI | 0.145033 | 0.047916 | 3.026811 | 0.0143 |

LNTOPN | -0.138509 | 0.121395 | -1.140977 | 0.2833 |

EXCR | 0.000991 | 0.000933 | 1.062281 | 0.3158 |

INF | -0.011867 | 0.002748 | -4.317816 | 0.0019 |

EC = LNRGDP - (0.1450*FDI -0.1385*LNTOPN + 0.0010*EXCR -0.0119 *INF + 0.0410*@TREND) | ||||

Null Hypothesis: | Obs | F-Statistic | Prob. |

|---|---|---|---|

FDI does not Granger Cause LNRGDP | 31 | 0.76778 | 0.4743 |

LNRGDP does not Granger Cause FDI | 2.46167 | 0.1049 | |

LNTOPN does not Granger Cause LNRGDP | 32 | 1.76515 | 0.1903 |

LNRGDP does not Granger Cause LNTOPN | 4.20997 | 0.0256 | |

EXCR does not Granger Cause LNRGDP | 32 | 0.18197 | 0.8346 |

LNRGDP does not Granger Cause EXCR | 1.13631 | 0.3359 | |

INF does not Granger Cause LNRGDP | 32 | 0.23395 | 0.7930 |

LNRGDP does not Granger Cause INF | 3.59131 | 0.0414 | |

LNTOPN does not Granger Cause FDI | 31 | 1.38297 | 0.2687 |

FDI does not Granger Cause LNTOPN | 0.13771 | 0.8720 | |

EXCR does not Granger Cause FDI | 31 | 2.19855 | 0.1312 |

FDI does not Granger Cause EXCR | 1.71398 | 0.1999 | |

INF does not Granger Cause FDI | 31 | 1.59240 | 0.2226 |

FDI does not Granger Cause INF | 3.22735 | 0.0560 | |

EXCR does not Granger Cause LNTOPN | 32 | 0.31637 | 0.7315 |

LNTOPN does not Granger Cause EXCR | 0.13125 | 0.8776 | |

INF does not Granger Cause LNTOPN | 32 | 1.97844 | 0.1578 |

LNTOPN does not Granger Cause INF | 0.29483 | 0.7470 | |

Breusch-Godfrey Serial Correlation LM Test: | |||

|---|---|---|---|

F-statistic | 4.279485 | Prob. F(2,7) | 0.1611 |

Obs*R-squared | 15.95286 | Prob. Chi-Square(2) | 0.0003 |

Heteroscedasticity Test: White | |||

|---|---|---|---|

F-statistic | 0.379522 | Prob. F(19,9) | 0.9639 |

Obs*R-squared | 12.89973 | Prob. Chi-Square(19) | 0.8437 |

Scaled explained SS | 1.279157 | Prob. Chi-Square(19) | 1.0000 |

5.1. Summary

5.2. Conclusion

5.3. Policy Recommendations

| [1] | A. A. Awe. (2013). impact of foreign direct investment on economic growth in Nigeria. |

| [2] | Adaramola, A. O. and Obisesan, O. G. (2015). Impact of Foreign Direct Investment on Nigerian Capital Market Development. International Journal of Academic Research in Accounting, Finance and Management Sciences, 5(1), pp103 – 103. |

| [3] | Adediran, O., George, E., Alege, P., & Obasaju, O. (2019). Is there any relationship between monetary policy tools and external credit-growth nexus in Nigeria? Cogent Economics & Finance, 7, 1625100. |

| [4] | Adeleke, K. M., S. O Olowe and F. O. Oladipo (2014). Impact of foreign direct investment on Nigeria economic growth, International Journal of Academic Research in Business and Social Sciences, 4(8). |

| [5] | Adigun, A. (2015). Sectoral Inflow of Foreign Direct Investment and Economic Growth in Nigeria. Journal of Economics and Sustainable Development, 6(17). |

| [6] | Alfarro, L. (2017). Gains from foreign direct investment: macro and micro approaches. World Bank Economic Review, 30, 2–15. |

| [7] | Agyemang, O., Gbettey, C., Gatsi, J., & Acquah, I. (2019). Country-level corporate governance and foreign direct investment in Africa. Corporate Governance, 19(5): 1133-1152. |

| [8] | Ajayi, S. I. (2006). FDI and economic development in Africa. A Paper presented at the ADB/AERC International [online]. |

| [9] | Akpan, S. B., Okon, U. E., & Udoka, S. J. (2014). Assessment of empirical relationships among remittances and agricultural productivity indicators in Nigeria (1970-2012). American Journal of Economics, 4(1), 52-61. |

| [10] | Alfaro, L. (2017). Gains from foreign direct investment: Macro and micro approaches. The World Bank Economic Review, 30(1): 2-15. |

| [11] | Alfaro, L. (2017). Multinational activity in emerging markets: How and when does foreign direct investment promote growth. Geography, location, and strategy. |

| [12] | Amoo, E. O. (2018). Introduction to special edition on Covenant University’s perspectives on Nigeria demography and achievement of SDGs-2030. Africa Population Studies, 32(1). |

| [13] | Anetor, F. O. (2019). Economic Growth effects of Private Capital inflow: A Structural VAR approach for Nigeria. Journal of Economics and Development, 21(1), 18-29. |

| [14] | Anfofum, A. A., Gambo, J. S., & Suleiman, T. (2013). Estimating the impact of foreign direct investment in Nigeria. International Journal of Humanities and Social Science, 3(17), 138-145. |

| [15] | Asiedu, E. (2002). On the determinants of foreign direct investment to developing countries: is Africa different? World development, 30(1), 107-119. |

| [16] | Awa, F. N. (2019). Influence of foreign direct investment on economic growth in Nigeria,2(6). |

| [17] | Awe, M. A. (2017). The role of real interest rates and savings in Nigeria. First Bank of Nigeria Quarterly Review, 1(2), 21-38. |

| [18] | Bakare-Aremu, T. A. (2015). Macroeconomic theory (ECO 718). Abuja: National Open University of Nigeria. |

| [19] | Balcerowicz L., (2014) Libértate §i dezvoltare. Economia piefei libere, Multiprint Publishing House, Iasi. |

| [20] | Basu, A., & Srinivasan, K. (2002). Foreign direct investment in Africa-Some case studies. |

| [21] | Blonigen, B. (1997). Firm specific assets and the link between exchange rates and foreign direct investment, American Economic Review 87, 448–465. |

| [22] | Botha, I. Botezatu, M. A. & Coanca, M. (2020). Innovative calculation model for evaluating regional sustainable development. Economic Computation and Economic Cybernetics Studies and Research, 54(3), 5–24. |

| [23] | Buckley, P. J., & Casson, M. (1976). A long-run theory of the multinational enterprise. In The future of the multinational enterprise (pp. 32-65). Palgrave Macmillan, London. |

| [24] | Buckley, P. J. and M. Casson (1976). The Future of the Multinational Enterprises. Macmillan, London. |

| [25] | Campos, N. F., & Kinoshita, Y. (2003). Why does FDI go where it goes? New evidence from the transition economies. International Monetary Fund. |

| [26] | Caves, R. E. 1971, "International corporations: The industrial economics of foreign investment", Economica, pp. 1-27. |

| [27] | Chappelow, J. (2019). Gross Domestic Product—GDP. Tomado de: https://www. investopedia. com/terms/g/gdp. asp. |

| [28] | Coase, R. H. (1991). The nature of the firm (1937). The Nature of the Firm. Origins, Evolution, and Development. New York, Oxford, 18, 33. |

| [29] | Cohen, B. (1975) Multinational Firms and Asian Exports. New Haven, CT: Yale University. |

| [30] | Danja, H. K. (2012). “Foreign Direct Investment and the Nigerian Economy”. American Journal of Economics, 2(3), 33 – 40. |

| [31] | Dunning, D. (2007). Self‐image motives and consumer behavior: How sacrosanct self‐beliefs sway preferences in the marketplace. Journal of consumer psychology, 17(4), 237-249. |

| [32] | Dunning, J. H. (1998). Towards an Eclectic Theory of International Production: Some Empirical Tests. Journal of International Business Studies, 21(1), 23-40. |

| [33] | Dunning, J. H. (2008). The eclectic paradigm as an envelope for economic and business theories of MNE activity. International Business Review, 9, 163–190. |

| [34] | Dunning, J. H. (1977). “Trade location of economic activity and the MNE: A search of an eclectic approach”, in B. Ohlin, P. O. Hesselborn and P. J. Wijkman (eds.), The International Allocation of Economic Activity. Macmillan, London. |

| [35] | Dunning, J. H. (1979). “Explaining changing patterns of international production: In defense of the eclectic theory”, Oxford Bulletin of Economics and Statistics, vol. 41, No. 4. |

| [36] | Dunning, J. H. (1980). “Towards an eclectic theory of international production”, Journal of International Business Studies, vol. 11, No. 1. |

| [37] | Dunning, J. H. (1988). “The eclectic paradigm of international production: A restatement and some possible extensions”, Journal of International Business Studies, vol. 19, No. 1. |

| [38] | Dunning, J. H. (1993). The Globalization of Business, Routledge, London. |

| [39] | Dunning, J. H. 1974, "The determinants of international production", Oxford economic papers, pp. 289-336. |

| [40] | Edwards, K. (1990). The interplay of affect and cognition in attitude formation and change. Journal of personality and social psychology, 59(2), 202. |

| [41] | Ehimare, A. (2011). The Effect of Exchange Rate and Inflation on Foreign Direct Investment and Its Relationship with Economic Growth in Nigeria. Annals of Dunărea de Jos University. Fascicle I: Economics and Applied Informatics, 1(1), 5–16. |

| [42] | Emmanuel, I. J. (2016). Effect of Foreign Direct Investment on Economic Growth in Nigeria. European Business and Management, 2(2), 40-46. |

| [43] | Esew, N. G., & Yaroson, E. (2014). Institutional quality and foreign direct investment (FDI) in Nigeria: A prognosis. IOSR Journal of humanities and social science, 19(6), 37-45. |

| [44] | Eze C. N. (2020) Foreign Direct Investment. A Panacea to National Economic Development in Nigeria? International Kindle Paperwhite, Munich GRIN Verlag. |

| [45] | Froot, K. and Stein, J. (1991). Exchange rates and FDI: an imperfect capital markets approach, Quarterly Journal of Economics 106, 1191–1127. |

| [46] | Giwa T. Babatunde A. Emmanuel O. George, Henry Okodua & Oluwasogo S. Adediran, (2020). Empirical analysis of the effects of foreign direct investment inflows on Nigerian Real economic growth: Implications for sustainable development goal-17, Cogent Social Sciences, 6: 1, 1727621, |

| [47] | Giwa, B. A., George, E. O., & Okodua, H. (2019). Causal nexus between foreign direct Investment, capital intensity, labour quality and economic growth in Nigeria. Proceedings of the 33rd International Business Information Management Association Conference, IBIMA 2019, |

| [48] | Granger, C. W. (1969). Investigating causal relations by econometric models and cross-spectral methods. Econometrica: journal of the Econometric Society, 424-438. |

| [49] | Grenada, Spain: Education Excellence and Innovation Management through Vision 2020 (pp. 7282–7289). |

| [50] | Gujarati, D. N., & Porter, D. C. (2009). Basic econometrics (international edition). New York: McGraw-Hills Inc. |

| [51] | Hammed Yinka Sabuur and Okunoye A. Ismaila. impact of foreign direct investment on economic growth overtimes in the Nigerian economy. 2021. |

| [52] | Haruna Danja, K. (2012). Foreign direct investment and the Nigerian economy. American Journal of Economics, 2(3), 33-40. |

| [53] | Hassen & Anis, O. (2012). Foreign direct investment (FDI) and economic growth: An approach in term of integration for the case of Tunisia. Journal of applied finance and banking, vol. 2, no. 4 pp 193-207. |

| [54] | Henisz, W. J. (2003). The power of the Buckley and Casson thesis: the ability to manage institutional idiosyncrasies. Journal of international business studies, 34(2), 173-184. |

| [55] | Iheanachor, Nkemdilim; Ozegbe, Azuka Elvis (2021): An assessment of foreign direct investment and sustainable development nexus: The Nigerian and Ghanaianperspectives, International Journal of Management, Economics and Social Sciences (IJMESS), ISSN 2304-1366, IJMESS International Publishers, Jersey City, NJ, Vol. 10, Iss. 1, pp. 49-67, |

| [56] | Isah, W. (2012). “Determinants of Foreign Direct Investment in Nigeria: An empirical Investigation”. (Unpublished Master’s thesis). Eastern Mediterranean University, Gazimagusa, North Cyprus. |

| [57] | Isah, W. (2016). Determinants of Foreign Direct Investment in Nigeria: An empirical Investigation. (Unpublished Master’s thesis). Eastern Mediterranean University, Gazimagusa, North Cyprus. |

| [58] | Iya, I. B., & Aminu, U. (2015). An investigation into the impact of domestic investment and foreign direct investment on economic growth in Nigeria. International Journal of Humanities Social Sciences and Education (IJHSSE), 2(7), 40-50. |

| [59] | Jaspersen, F. Z., Aylward, A. H., & Knox, A. D. (2000). Risk and private investment: Africa compared with other developing areas. In Investment and risk in Africa (pp. 71-95). Palgrave Macmillan, London. |

| [60] | Jhingan, M. L. (2007). The economics of development and planning (3 ed.). Delhi: Vrinda Publications (P) Ltd. |

| [61] | John, E. I. (2016) Effect of Foreign Direct Investment on Economic Growth in Nigeria. European Business & Management, 2, 40-46. |

| [62] | Khan, L., Arif, I., & Raza, S. A. (2021). Capital Flow, Capital Control, and Economic Growth: Evidence from Developed & Developing Economies. Journal of Accounting and Finance in Emerging Economies, 7(2), 467-482. |

| [63] | Kindleberger, C. P. 1969, "American business abroad", The International Executive, vol. 11, no. 2, pp. 11-12. |

| [64] | Kolawole, B. O. (2013). Foreign assistance and economic growth in Nigeria: The two-gap model framework. American international journal of contemporary research, 3(10), 153-160. |

| [65] | Koojaroenprasit, B. (2012) The Impact of Foreign Direct Investment on Economic Growth: A Case Study of South Korea. International Journal of Business and Social Science, 3, 8-18. |

| [66] | Kurtishi-Kastrati, S. (2013). Impact of FDI on economic growth: An overview of the main theories of FDI and empirical research. European Scientific Journal, 9(7). |

| [67] | Lamfalussy, Alexandre. 1961b. Money Substitutes and Monetary Policy. The Banker, January, CXI (419): 44-50. |

| [68] | Latorre, G. (2008). Walls of empowerment: Chicana/o indigenist murals of California. University of Texas Press. |

| [69] | Balcerowicz, L. (Ed.). (2014). Puzzles of economic growth. World Bank Publications. |

| [70] | Louzi, B. M. and Abadi, A. (2011) The Impact of Foreign Direct Investment on Economic Growth in Jordan. IJRRAS, 8, 253-258. |

| [71] | Lyndon M. Etale, Ayaundu E. Sawyerr. (2020) “Inventory Management and Financial Performance of NSE Listed GLAXOSMITHKLINE Consumer Nigeria PLC”; United Kingdom ISSN 2348 0386 Vol. VIII, Issue 6, June 2020. |

| [72] | Mahmoodi, M., & Mahmoodi, E. (2016). Foreign direct investment, exports and economic growth: evidence from two panels of developing countries. Economic Research EkonomskaIstrazivanja, 29(1), 938–949. |

| [73] | Matthew, O. H., & Johnson, A. T. A. N. (2013). An Investigation of the Impact of Foreign Direct Investment on Economic Growth in Nigeria: A Rigorous Approach. Journal of Poverty, Investment and Development, 3, 33-41. |

| [74] | Mody, A., & Srinivasan, K. (1998). Japanese and US firms as foreign investors: do they march to the same tune? Canadian journal of economics, 778-799. |

| [75] | Mokuolu, J. O. (2018). Effect of Exchange Rate and Interest Rate on FDI And Its Relationship with Economic Growth in Nigeria. 33–47. |

| [76] | Montiel, P. J., & Agénor, P. R. (2008). Development macroeconomics. Princeton University Press. |

| [77] | Muchlinski, T. E. (1995). Using cognitive coaching to model metacognition during instruction (Doctoral dissertation, The University of North Carolina at Chapel Hill). |

| [78] | Njogu, B. O. (2013). “Foreign Direct Investment Determinants in Pre-and Deregulated Nigerian Economy”. (Unpublished doctoral dissertation). University of Nigeria Nsukka, Enugu, Nigeria. |

| [79] | Nsofor, E., & Takon, S. (2017). Impact of foreign direct investment on economic growth: empirical evidence from nigeria, 1985-2016. European Journal of Economic and Financial Research, 2(6). |

| [80] | Nsofor, E. S., Takon, S. M., Ugwuegbe, S. U. (2017). Modeling Exchange Rate Volatility and Economic Growth in Nigeria. Noble International Journal of Economics and Financial Research, 2(6): 88-97. |

| [81] | Nyoni, T., & Bonga, W. G. (2018). Anatomy of the small & medium enterprises (SMEs) critical success factors (CSFs) in Zimbabwe: Introducing the 3E model. Dynamic Research Journals' Journal of Business & Management (DRJ-JBM), 1(2), 01-18. |

| [82] | Odishika, V. A. (2017). Development economics I. Lagos: National Open University of Nigeria (NOUN). |

| [83] | Ogu, C. (2020). Foreign direct investment and exchange rate in Nigeria. January 2019. Okon, J. U., Jacob, O. A., &Chuku, A. C. (2011). Foreign Direct Investment and Economic Growth in Nigeria: An Analysis of the EndogenenousEfects, 4(3), 53 – 66. |

| [84] | Okumoko, T. P and Karimo, T. M (2015). Foreign Direct Investment and Economic Growth in Nigeria: An analysis of the endogenous effects. International Journal of Management and economics invention Vol. 1(1): pp. 45-64. |

| [85] | Olajide, O. T. (2004). Theories of Economic Development and Planning. Lagos: Punmark Nigeri Limited, vol. 6. |

| [86] | Olokoyo, F. O. (2012). Foreign direct investment and economic growth: A case of Nigeria. BVIMSR’S Journal of Management Research, 4(1), 1-23. |

| [87] | Onuoha, C. B., and Orogwu, U. O. (2013). “The Determinants of Foreign Direct Investment (FDI) and the Nigerian Economy”. American International Journal of Contemporary Research, 3(11), 165 – 172. |

| [88] | Oseghale, B. D and Amonkhienan, E. E (1987). “Foreign debt, Oil Export, Direct Foreign Investment (1960 – 1984”). The Nigerian Journal of Economic and Social Studies, 29(3), 359 – 80. |

| [89] | Osemene, O. F., Kolawole, K. D., &Olanipekun, I. D. (2019). Determinants of FDI and Its Causal Effect on Economic Growth in Nigeria. KJBM, 8(1). |

| [90] | Oyedokun, G. E., & Ajose, K. (2018). Domestic investment and economic growth in Nigeria: an empirical investigation. International Journal of Business and Social Science, 9(2), 130-138. |

| [91] | Oyegoke, O. E., & Aras, O. N. (2021). Impact of Foreign Direct Investment on Economic Growth in Nigeria. Journal of Management, Economics and Industrial Organization, 5(1), 21-38. |

| [92] | Pesaran, H. H., & Shin, Y. (1998). Generalized impulse response analysis in linear multivariate models. Economics letters, 58(1), 17-29. |

| [93] | Pesaran, M. H. (1997). The role of economic theory in modelling the long run. The economic journal, 107(440), 178-191. |

| [94] | Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of applied econometrics, 16(3), 289-326. |

| [95] | Piętak, Ł. (2014). Review of theories and models of economic growth. Comparative Economic Research, 17(1), 45-60. |

| [96] | Pigato, M. (2001). Foreign direct investment in Africa: old tales and new evidence. Washington, D. C: The World Bank. |

| [97] | Romer, P. M. (2009). Beyond the Knowledge. Knowledge and strategy, 69. |

| [98] | Schneider, F., & Frey, B. S. (1985). Economic and political determinants of foreign direct investment. World development, 13(2), 161-175. |

| [99] | Sekunmade J. O (2020) investigates Foreign Direct Investment, Economic Freedom and Economic Growth of Nigeria between 1995 and 2018. |

| [100] | Shuaib, I. M., Dania, E. N., Imaogene, I., & Pogoson, O. O. (2015). The Impact of Foreign Direct Investment (FDI) on the Growth of the Nigerian Economy. International Journal of Research in Business Studies and Management, 11(3): 121-143. |

| [101] | Simaionescu, M., & Naros, M. S. (2019). The role of foreign direct investment in human capital Formation for a competitive lobour market. Management Research and Practice, 11(1), 5–14. |

| [102] | Sokang, K. (2018). The Impact of Foreign Direct Investment on the Economic Growth in Cambodia: Empirical Evidence. International Journal of Innovation and Economic Development, 4(5), 31–38. |

| [103] | Solow, R. M. (1956). A contribution to the theory of economic growth. The quarterly journal of economics, 70(1), 65-94. |

| [104] | Sunde, T. (2017). Foreign direct investment, exports and economic growth: ADRL and causality Analysis for South Africa. Research in International Business and Finance, 41(May), 434- 444. |

| [105] | Todaro, M. P., & Smith, S. C. (2011). Economic development (11th ed.). England: Pearson Education Ltd. |

| [106] | Tsai, P. L. (1994). Determinants of foreign direct investment and its impact on economic growth. Journal of economic development, 19(1), 137-163. |

| [107] | UNCTAD (2018) United Nations Conference on Trade and Development. World Investment Report. |

| [108] | UNCTAD (2019) United Nations Conference on Trade and Development. World Investment Report. |

| [109] | UNCTAD. (1999). World Investment Report 1999: Foreign direct investment and the challenge of development. In United Nations Conference on Trade and Development. Geneva: United Nations. |

| [110] | Uwubanmwen, A. E., & Ogiemudia, O. A. (2016, March). Foreign Direct Investment and Economic Growth: Evidence from Nigeria. International Journal of Business and Social Science, 17(3), 1-15. |

| [111] | Vaitsos, C. V. (1974). Income distribution and welfare considerations. Economic analysis and the Multinational enterprise, 298-341. |

| [112] | Vernon, R. (1966). “International investment and international trade in the product cycle”, Quarterly Journal of Economics, vol. 80, No. 2. |

| [113] | Vernon, R. (1979). The product cycle hypothesis in a new international environment. Oxford Bulletin of economics and statistics, 41(4), 255-267. |

| [114] | Wilhelms, S. K. & Witter, M. S. D. 1998, Foreign direct investment and its determinants in emerging Economies, United States Agency for International Development, Bureau for Africa, Office of Sustainable Development. |

| [115] | Zhang, K. H. (2001), “Does foreign direct investment promote economic growth? Evidence from East Asia and Latin America”. Contemporary Economic Policy, 19(2, April): 175–85. |

APA Style

Amade, M. A., Oyigebe, P. L. (2024). Foreign Direct Investment and the Nigerian Economy: An Empirical Analysis . International Journal of Economic Behavior and Organization, 12(2), 46-66. https://doi.org/10.11648/j.ijebo.20241202.11

ACS Style

Amade, M. A.; Oyigebe, P. L. Foreign Direct Investment and the Nigerian Economy: An Empirical Analysis . Int. J. Econ. Behav. Organ. 2024, 12(2), 46-66. doi: 10.11648/j.ijebo.20241202.11

AMA Style

Amade MA, Oyigebe PL. Foreign Direct Investment and the Nigerian Economy: An Empirical Analysis . Int J Econ Behav Organ. 2024;12(2):46-66. doi: 10.11648/j.ijebo.20241202.11

@article{10.11648/j.ijebo.20241202.11,

author = {Muhammed Akpai Amade and Peter Luke Oyigebe},

title = {Foreign Direct Investment and the Nigerian Economy: An Empirical Analysis

},

journal = {International Journal of Economic Behavior and Organization},

volume = {12},

number = {2},

pages = {46-66},

doi = {10.11648/j.ijebo.20241202.11},

url = {https://doi.org/10.11648/j.ijebo.20241202.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijebo.20241202.11},

abstract = {The primary motive of this paper was to investigate the impact of Foreign Direct Investment on economic growth of Nigeria from 1985 to 2022. Ex – post facto research design was carefully carried out; annual time series data were extracted from Central Bank of Nigeria Statistical Bulletin of 2021 and World Development Indicator. Real Gross Domestic Product (RGDP) was used as the dependent variable proxy for economic growth. Foreign Direct Investment (FDI), Exchange Rate (EXCR), Trade Openness (TOPN) and Inflation (INF) all denoted for explanatory variables of the study. The estimated coefficients of the variables under study displayed that all the variables are integrated of the same order 1(1) exception of Foreign Direct Investment which was integrated of order 1(0). The bound test conducted showed that there is proof of the presence of a long run correlation among the variables used while the causality test clearly showed that FDI granger causes economic growth in Nigeria under review. Other diagnostic tests seen in this paper are unit root test, descriptive statistics, correlation coefficient matrix, Cointegration test and test of Normality respectively, and they long-established the validity and reliability of the model used. Based on the inferential results revealed by the research work, the paper came up with recommendation that government should improve the investment climate for both domestic and foreign investors through adequate infrastructural development, soft loans and tax holidays.

},

year = {2024}

}

TY - JOUR T1 - Foreign Direct Investment and the Nigerian Economy: An Empirical Analysis AU - Muhammed Akpai Amade AU - Peter Luke Oyigebe Y1 - 2024/04/02 PY - 2024 N1 - https://doi.org/10.11648/j.ijebo.20241202.11 DO - 10.11648/j.ijebo.20241202.11 T2 - International Journal of Economic Behavior and Organization JF - International Journal of Economic Behavior and Organization JO - International Journal of Economic Behavior and Organization SP - 46 EP - 66 PB - Science Publishing Group SN - 2328-7616 UR - https://doi.org/10.11648/j.ijebo.20241202.11 AB - The primary motive of this paper was to investigate the impact of Foreign Direct Investment on economic growth of Nigeria from 1985 to 2022. Ex – post facto research design was carefully carried out; annual time series data were extracted from Central Bank of Nigeria Statistical Bulletin of 2021 and World Development Indicator. Real Gross Domestic Product (RGDP) was used as the dependent variable proxy for economic growth. Foreign Direct Investment (FDI), Exchange Rate (EXCR), Trade Openness (TOPN) and Inflation (INF) all denoted for explanatory variables of the study. The estimated coefficients of the variables under study displayed that all the variables are integrated of the same order 1(1) exception of Foreign Direct Investment which was integrated of order 1(0). The bound test conducted showed that there is proof of the presence of a long run correlation among the variables used while the causality test clearly showed that FDI granger causes economic growth in Nigeria under review. Other diagnostic tests seen in this paper are unit root test, descriptive statistics, correlation coefficient matrix, Cointegration test and test of Normality respectively, and they long-established the validity and reliability of the model used. Based on the inferential results revealed by the research work, the paper came up with recommendation that government should improve the investment climate for both domestic and foreign investors through adequate infrastructural development, soft loans and tax holidays. VL - 12 IS - 2 ER -

Department of Economics, Federal University, Lokoja, Nigeria

Department of Political Science, Federal University, Lokoja, Nigeria

Information