1. Introduction

In today’s dynamic and highly competitive business environment, organizations rely on the efficiency and effectiveness of their employees to maintain sustainable growth and achieve strategic objectives. Among various roles in business operations, accounting personnel play a crucial role in ensuring financial integrity, compliance, and decision-making processes. However, the increasing complexity of financial regulations, technological advancements, and the demand for accuracy in financial reporting place significant pressure on accounting professionals. These challenges necessitate key personal attributes such as resilience and motivation to sustain high in-role performance in large-scale business organizations. The execution of assigned tasks, responsibilities, and duties, is vital to organizational efficiency and sustainability. However, achieving optimal performance in accounting roles requires more than just technical expertise and professional training; personal motivation is a significant determinant of how well accountants perform in their designated roles. Accounting is the significant recording, classifying, summarizing, and interpretation of money, transactions, and events that have financial characteristics

. Since quality and timely financial reporting is of topmost importance and uncompromised in business, it is the duty and responsibility of accounting personnel in any business organisation to ensure that financial reports are made available to management as at when needed.

Accounting personnel are goal-oriented individuals who are responsible for providing financial information for decision-making to the users

| [10] | Joshua, S. & Ugwoke, E. O. (2022). Skills improvement needs of accounting personnel in Federal Capital Territory, Abuja, Nigeria. International Journal of Accounting and Financial Management Research (IJAFMR), 12(2), 25-40. |

[10]

. The authors further stated that accounting personnel are important assets of any business organisation because of their functions. Accounting personnel is a qualified employee who collects, organizes, analyzes, and presents financial information to those who need it at the right time

| [17] | Masten, A. S. (2018). Resilience theory and research on children and families: Past, present, and promise. Journal of Family Theory & Review, 10(1), 12-31. |

[17]

. In the context of this study, accounting personnel can be defined as individuals or employees who have acquired the knowledge and skills through certified educational programmes such as graduates of accountancy and business education (accounting) to carry out accounting and financial tasks in organisations. Furthermore, accounting personnel refers to an individual responsible for managing financial transactions, maintaining records, ensuring compliance with financial regulations, and preparing financial reports within an organization

| [1] | Abah, F. (2024). Understanding How Experienced Financial Accounting Leaders Instill and Maintain Ethics in Financial Accounting Processes in Their Respective Organizations (Doctoral dissertation, Capella University). |

[1]

. These professionals play a crucial role in business operations by providing accurate and timely financial information that supports decision-making, strategic planning, and regulatory compliance. In large-scale business organizations, accounting personnel play a pivotal role in financial management and corporate governance. Their work ensures transparency, supports operational efficiency, and enhances investor confidence. This is done by maintaining accurate records and ensuring compliance, they contribute to the financial sustainability and success of an organization. Accounting personnel, especially in large-scale business organisations, due to large volume of work seems to experience professional challenges such as work stress, rigorous demand from technological advancements, work-life imbalance and loss, high workloads, among others which require their personal resilience and motivation to be able to cope and perform proficiently and effectively.

Personal resilience may be an important behavioural outcome that if developed, may influence productive performance of accounting personnel in carrying out their jobs and responsibilities. Resilient accounting personnel can effectively manage tight deadlines, handle financial complexities, and navigate organizational changes without compromising performance. Personal resilience can be defined as a dynamic and adaptive system an individual possesses which enables him/her capable of adjusting to challenges and adversities that pose a threat to the viability, the function, or the development of that individual

| [17] | Masten, A. S. (2018). Resilience theory and research on children and families: Past, present, and promise. Journal of Family Theory & Review, 10(1), 12-31. |

[17]

. Personal resilience refers to an individual’s ability to adapt to stress, overcome adversity, and maintain productivity despite workplace challenges. In essence, personal resilience emphasizes the proactive nature and suggesting that individuals with high levels of personal resilience possess an inherent capacity to adjust and respond effectively to various adversities or difficulties. In the same vein, personal resilience is the psychological qualities that enhance an individual's ability to recover, bounce back from setbacks or turn adversity into an advantage and make them become stronger

| [13] | Khan, E., Sadiq, N., Fatima, A., Deen, N., Muneer, R., Iftikhar, S., & Kashif, M. (2023). Relationship of resilience and anxiety with injury prevention programs in pakistani footballers: relationship of resilience and anxiety with injury. The Therapist (Journal of Therapies & Amp; Rehabilitation Sciences), 4(1). https://doi.org/10.54393/tt.v4i1.80 |

[13]

. Operationally, an accounting personnel’s personal resilience is the ability to work through difficulties, emotional pain and stress while performing his professional duties and responsibilities in the organisation and come out with a desired result. Individuals who possess greater levels of resilience are minimally challenged in their workplace

| [15] | Liman, P., Xiu, W., Fan, L., Tingting, F., Huaruo, C., & Ya, W. (2021). The relationship between college students’ resilience and career decision-making difficulties: the mediating role of career adaptability. Psychology, 12, 872-886, https://doi.org/10.4236/psych.2021.126053 |

[15]

. The resilient employees typically possess positive attitudes about life, demonstrate eagerness to adapt to new experiences and possess the ability to control themselves. Since resilience is mainly positive in nature, it can predict an employees’ work motivation.

Similarly, motivation is a critical determinant of job engagement and productivity. Motivated accountants are more likely to demonstrate commitment, accuracy, and proactive problem-solving, all of which contribute to superior in-role performance. However, achieving optimal performance in accounting roles requires more than just technical expertise and professional training; personal motivation is a significant determinant of how well accountants perform in their designated roles

| [13] | Khan, E., Sadiq, N., Fatima, A., Deen, N., Muneer, R., Iftikhar, S., & Kashif, M. (2023). Relationship of resilience and anxiety with injury prevention programs in pakistani footballers: relationship of resilience and anxiety with injury. The Therapist (Journal of Therapies & Amp; Rehabilitation Sciences), 4(1). https://doi.org/10.54393/tt.v4i1.80 |

[13]

. Personal motivation at work place has a significant positive impact on employee overall performance including in-role performance

| [22] | Rifa’i, A., Muchlis, M., & Susanto, B. F. (2024). Building meaningful work through inclusive leadership: the role of psychological safety. In International Conference of Business and Social Sciences (pp. 974-987). |

[22]

. Similarly, a study investigated the impact of competence, compensation, and motivation on employee performance, with job satisfaction as an intervening variable

| [12] | Kaur, T., & Mandal, S. (2024). Exploring role transitions and conflicts on work disengagement under varying settings: the moderating role of individual resilience. International Journal of Conflict Management, 35(3), 488-507. |

[12]

. The study highlighted the importance of job satisfaction in mediating the relationship between these factors and employee performance in an organization. Likewise, a study explored the effects of intrinsic and extrinsic motivation on employee performance, with job satisfaction as an intervening variable

| [26] | Yusuf, M. (2021). The effects of the intrinsic motivation and extrinsic motivation on employee performance with job satisfaction as an intervening variable at PT. Alwi Assegaf Palembang. Mbia, 20(1), 18-31. |

[26]

. The study revealed that job satisfaction did not mediate the relationship between motivation and performance. The accounting profession, characterized by rigorous standards, complex financial analyses, and strict regulatory frameworks, demands high levels of diligence, accuracy, and ethical responsibility. As such, understanding how personal motivation influences the in-role performance of accounting personnel in large-scale organizations is essential for both management and policymakers in fostering a highly productive and engaged workforce. Incidentally, like any other employee, an accounting personnel’s personal motivation towards work aspirations can be further shaped by their abilities to adapt to difficult situations and conditions while performing their overall job duties and responsibilities.

In-role performance, a key measure of workplace effectiveness, encompasses an employee’s ability to fulfil their job responsibilities efficiently and contribute to organizational success. The in-role performance (IRP) of an employee is required behaviours needed to be demonstrated by employees of an organisation for a given job. These behaviours are directly related to the essential duties and tasks of the individual carrying out the job in an organisation. In-role performance are employees’ behaviours that are described and reflected as part of their job and responsibilities which are indicated in their official schedule in the organisation

| [25] | Yanhan, Z. (2013). Individual behaviour: In-role and extra-role. International Journal of Business Administration. 4(1). www.sciedu.ca/ijba |

[25]

. Also, in-role performance can be defined as the essential behaviours that are expected from the employee for the successful accomplishment of the job duties and responsibilities

| [2] | Adnan, A., Anila, K. & Sultan. S (2019). Perceived authentic leadership in relation to in-role and extra-role performance: A job demands and resources perspective. Journal of Behavioural Sciences. 29(1), 115-124. |

[2]

. In this study, in-role performance (IRP) performance are the job duties, tasks and responsibilities assigned to accounting personnel to carry out for the achievement of goals and objectives of large-scale business organisations. In-role performance (IRP) is important for organisational effectiveness and productivity, as well as for employees’ evaluation and reward. However, it is not enough for accounting personnel to carry out their job requirements and job tasks effectively and efficiently in large-scale business organisation without considering their performance which is essential to achieving the goals and objectives of the organisation.

A study

| [17] | Masten, A. S. (2018). Resilience theory and research on children and families: Past, present, and promise. Journal of Family Theory & Review, 10(1), 12-31. |

[17]

highlighted the importance of supportive management in the success of performance management. The study emphasized the need for organisations to change the way they engage with employees and manage performance to ensure it adds value to all stakeholders. Also, another study

| [8] | González-Morales, M. G., & Neves, P. (2015). When stressors make you work: Mechanisms linking challenge stressors to performance. Work & Stress, 29(3), 213-229. |

[8]

examined how challenge stressors are connected to performance of workers in an organisation. The mediating role of increased psychosomatic distress was supported only for the relationship between threat appraisal and in-role performance of workers. The authors explained how leader behavioural integrity facilitates employee’s in-role performance and the boundary conditions determining the correlation between leader behavioural integrity and employee in-role performance. Certainly, engaging in in-role performance empowers employees to approach tasks with creativity, generating innovative and practical solutions to challenges

| [27] | Zhang, X., & Bartol, K. M. (2010). The influence of creative process engagement on employee creative performance and overall job performance: A curvilinear assessment. Journal of Applied psychology, 95(5), 862. |

[27]

. Similarly, accounting personnel are not adequately utilizing techniques that could facilitate fraud detection in large-scale business organisations as required to combat the menace

| [6] | Ezenwafor, J. I., & Mgbe, B. N. (2019). Perception of SMES managers in Anambra State on the extent employees’ participation in decision making improve their work performance. NAU Journal of Technology and Vocational Education, 3(1), 116-127. |

[6]

. Certainly, engaging in in-role performance empowers employees to approach tasks with creativity, generating innovative and practical solutions to challenges

| [21] | Rashid, M., Tasmin, R., Qureshi, M. I., & Shafiq, M. (2017). Relationship of servant leadership with employee in-role and extra-role performance in GLC’S of Malaysia. City University Research Journal, 1(NIL), 88-95. |

[21]

. The skills and knowledge acquired through participation in creative endeavours in one domain can subsequently enhance an employee's performance in other areas

| [5] | Eshleman, J. D., & Guo, P. (2014). Abnormal audit fees and audit quality: The importance of considering managerial incentives in tests of earnings management. Auditing: a journal of practice & theory, 33(1), 117-138. |

[5]

, thereby contributing to elevated levels of in-role performance. In-role performance is considered as an employee's formal conduct aligned with their role requirements, encompassing the fundamental job duties and tasks outlined in the job description

| [21] | Rashid, M., Tasmin, R., Qureshi, M. I., & Shafiq, M. (2017). Relationship of servant leadership with employee in-role and extra-role performance in GLC’S of Malaysia. City University Research Journal, 1(NIL), 88-95. |

[21]

.

The global concept of large-scale business organisations is an important tool that needs to be exploited not only for providing good and services for people but also for boosting the economy of a countries around the world. A study

noted that large-scale business organisations refer to companies or enterprises that operates on an extensive scale, widespread operations, and often a global reach encompassing a significant workforce of 250 or more with typically substantial assets, revenues, market influence and capital of more than $1 billion in gross receipts. However, large-scale business organisations are profit-oriented establishment meant to provide services and production in a large quantity for customers and clients. Large-scale business organisations as companies and firms that can provide goods and services in large quantity because of the large number of skilled workers, increase in profit margin and high market demand

| [18] | Matejun, M. (2017). Characteristic features of small business and large firms: An empirical comparative study. Journal of Administrative and Business Studies (JABS), 3(4), 192-203, https://doi.org/12.20474/jabs-3.4.4 |

[18]

. The author also opined that Large-scale business organisations are enterprises that are characterized by having huge raw material needs, huge infrastructure, high manpower and large capital requirements. Similarly, large-scale business organisations are divergent in nature with their definitions revolving around the number of employees, available assets, annual income, and revenue, net-worth, and volume of profit of the business organisation

| [14] | Kingsley, A. (2018). Implementing forensic management in large scale business organisations. Global Journal of Management and Business Research: Administration and Management, 18(6). |

[14]

. The author further noted that a large-scale business organisation involves personnel that possess high level of managerial and administrative skills to carry out its activities with maximum business productivity. In the context of this study, large-scale business organisations can be referred to as enterprises, companies or industries that have large number of skilled and unskilled workforce, and professional manpower who control the resources of the enterprise for the purpose of meeting the business goals.

Organizations invest heavily in employee motivation through financial incentives, career development programs, and performance appraisals, yet disparities in job performance among accounting personnel persist. Some employees thrive under pressure, demonstrating high levels of accuracy and diligence, while others struggle despite having access to the same organizational resources. Despite the significance of accounting personnel in organizational success, many face challenges such as high workload, stress, and strict regulatory requirements. Without adequate resilience and motivation, performance levels decline, leading to financial discrepancies and inefficiencies. This suggests that personal resilience and motivation can act as determinants that translates into job performance. Without a clear understanding of how motivation and resilience interact to influence in-role performance, organizations may face challenges in designing effective employee support systems. Therefore, this study seeks to examine the relationship between personal resilience and motivation in shaping the job performance of accounting personnel in large-scale business organizations.

1.1. Statement of the Problem

The performance of accounting personnel in large-scale business organizations is crucial for financial accuracy, regulatory compliance, and overall corporate success. However, in the face of increasing job demands, financial pressures, and evolving regulatory frameworks, accounting professionals often encounter stress, job fatigue, and ethical dilemmas that may affect their performance. While personal motivation plays a significant role in enhancing employee productivity, motivation alone may not be sufficient to sustain high levels of job performance. Personal resilience, which refers to an individual’s ability to adapt, recover from challenges, and maintain performance under pressure, has emerged as a critical factor in ensuring consistent and high-quality job performance. Despite this, limited research has explored the combined influence of personal resilience and motivation on the in-role performance of accounting personnel, particularly in large-scale organizations where work complexities and expectations are high.

1.2. Research Objectives

This study aims to examine how personal resilience and motivation contribute to the in-role performance of accounting personnel in large-scale business organizations. the study will provide insights into how organizations can foster resilience and motivation through targeted policies, training, and workplace culture to enhance employee performance.

1) To examine the correlation between personal resilience and in-role performance of accounting personnel.

2) To examine the correlation between motivation and the in-role performance of accounting personnel.

3) To examine the combined correlation of resilience and motivation on in-role performance accounting personnel.

1.3. Null Hypotheses

1) There is no significant correlation between personal resilience and in-role performance of accounting personnel.

2) There is no significant correlation between motivation and the in-role performance of accounting personnel.

3) There is no significant combined correlation of resilience and motivation on in-role performance accounting personnel.

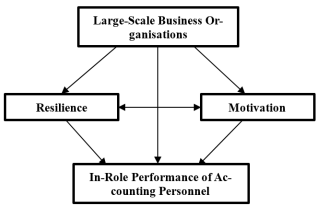

1.4. Conceptual Model

The conceptual model for this study examines how personal resilience and motivation influence the in-role performance of accounting personnel in large-scale business organizations. Personal resilience represents an individual’s ability to adapt to challenges, manage stress, and maintain productivity despite workplace pressures. Motivation, which includes both intrinsic factors (such as personal drive and job satisfaction) and extrinsic factors (such as financial incentives and recognition), plays a crucial role in determining employees’ engagement and commitment to their roles. These two independent variables directly impact in-role performance, which refers to how effectively accounting personnel fulfil their job responsibilities, including accuracy in financial reporting, compliance with regulations, and problem-solving skills. This model provides a framework for understanding how psychological and motivational factors contribute to employee effectiveness and organizational success.

Figure 1. Correlation of Personal Resilience, Motivation and In-Role Performance of Accounting Personnel.

3. Data Analysis and Results Presentation

HO1: There is no significant correlation between personal resilience and in-role performance of accounting personnel.

Table 1. Linear Regression Analysis of no Significant Correlation between Personal Resilience and In-Role Performance of Accounting Personnel.

Personal Resilience | |

Source | B | SEB | β | t | Sig. | Remarks |

In-Role Performance (Constant) | .339 | .379 | | 5.642 | .000 | S |

Personal Resilience | .468 | .506 | .734 | 3.460 | .001 | S |

R2.655 | |

F 1.973** | |

Table 1 presents the results of the linear regression analysis (LRA) on whether personal resilience significantly correlates with the in-role performance of accounting personnel in large-scale business organisations in North-Central Nigeria. The regression coefficient (B) for personal resilience is .468, with a standard error of .506. The standardized beta coefficient (β) is .734, indicating a strong positive correlation of personal resilience with in-role performance. The t-value for personal resilience is 3.460, with a significance level (Sig.) of .001. This significance level is well below the alpha level of .05, indicating that personal resilience statistically and significantly correlates with in-role performance of accounting personnel studied. This means that personal resilience significantly correlates with the in-role performance of accounting personnel. The constant (intercept) for the model is .339, with a t-value of 5.642 and a significance level of .001, suggesting that the model fits the data well. The R-squared (R

2) value of .655 indicates that approximately 65.5% of the variance in in-role performance can be explained by personal resilience of accounting personnel in large-scale business organisations in North-Central Nigeria. Based on the above results, hypothesis one is rejected showing there is significant correlation between personal resilience and in-role performance.

HO2: There is no significant correlation between personal motivation and the in-role performance of accounting personnel.

Table 2. Linear Regression Analysis of no Significant Correlation between Personal Motivation and In-Role Performance of Accounting Personnel.

Personal Motivation | |

Source | B | SE | β | t | Sig. | Remarks |

In-Role Performance (Constant) | 1.674 | .194 | | 8.632 | .000 | S |

Personal Motivation | .494 | .054 | .539 | 9.201 | .000 | S |

R2.690 | |

F 84.651** | |

Table 2 presents the results of linear regression analysis examining the correlation of personal motivation and the in-role performance of accounting personnel in large-scale business organisations in North-Central Nigeria, in line with hypothesis two. The result reveals that personal motivation significantly and positively correlates with in-role performance. The regression coefficient (B) for personal motivation is 0.494, with a standard error of 0.054, and a standardized beta coefficient (β) of 0.539. The t-value for personal motivation is 9.201, which is statistically significant at p <.01, indicating a strong positive relationship between personal motivation and in-role performance. The constant (In-Role Performance) in the regression equation is 1.674, with a standard error of 0.194, and is significant at p <.01 (t = 8.632), suggesting that the model is well-fitted. The R-squared (R²) value of 0.690 indicates that 69% of the variance in in-role performance can be explained by personal motivation. Based on these results, hypothesis two is rejected, indicating that personal motivation significantly correlates with the in-role performance of accounting personnel in large-scale business organisations in North-Central Nigeria. This underscores the importance of promoting personal motivation among accounting personnel to enhance their in-role performance.

HO3: There is no significant combined correlation of personal resilience and motivation with in-role performance accounting personnel.

Table 3. Linear Regression Analysis of no Significant Combined Correlation of Personal Resilience and Motivation on In-Role Performance Accounting Personnel.

Model | | | | | | 95% CI for B | | | |

B | SE | β | t | P | Upper | Lower | Tolerance | VIF | Remarks |

1 | In-Role Performance (Constant) | 2.139 | .379 | | 5.642 | .000 | 1.392 | 2.887 | | | |

2 | Personal Resilience | .731 | .696 | .783 | 1.358 | .001 | .259 | .320 | .914 | 1.094 | S |

| Personal Motivation | .771 | .856 | .814 | 8.416 | .000 | .361 | .582 | .914 | 1.094 | S |

| R2.797 | | | | | |

| F 43.420** | | | | | |

Note: ** p <.01

The Linear regression analysis in

Table 3 explores the hypothesis regarding the combined correlation of personal resilience and motivation with in-role performance accounting personnel of accounting personnel in large-scale business organisations. The analysis presented met the assumptions of collinearity in that the tolerance values accounted for 0.914 respectively for personal resilience and personal motivation of accounting personal on their in-role performance in large-scale business organizations. While the value inflation factor (VIF) accounted for 1.094 respectively, indicating that the problem of collinearity does not exist between for personal resilience and personal motivation of accounting personal. The analysis reveals compelling evidence that the combination of these factors significantly correlates with in-role performance. In the first model, personal resilience shows a significant positive correlation with in-role performance ((B = 0.731, SE = 0.696,

β = 0.834, t = 1.358, P = 0.001), indicating that accounting personnel with higher levels of personal resilience tend to perform better in their roles and responsibilities. While the second model of personal motivation shows significance (B = 0.771, SE = 0.856,

β = 0.814, t = 8.416, P = 0.000) which shows a positive correlation on in-role performance. The models both show that R² value is 0.797, indicating that 79.7% of the variance in in-role performance can be explained by personal resilience and motivation. These results suggest that personal resilience and personal motivation collectively have a significant correlation with the in-role performance of accounting personnel in large-scale business organisations. Hence, organisations looking to enhance the performance of their employees should consider personal resilience and motivation of their employees to promote these attributes in their workforce.

4. Discussion of Findings

The research hypothesis one sought to determine a no significance correlation between personal resilience and in-role performance of accounting personnel. The results revealed a significant and positive correlation between personal resilience and in-role performance of accounting personal. This suggests that higher levels of personal resilience are associated with better in-role performance of accounting personnel. These findings resonate with existing literature. A study was conducted and found that resilience is linked to performance, with workers' well-being mediating this relationship

| [4] | Cantante-Rodrigues, F., Lopes, S., Sabino, A., Pimentel, L., & Dias, P. C. (2021). The association between resilience and performance: The mediating role of workers’ well-being. Psychological Studies, 66(1), 36-48. |

[4]

. Also, a study showed that resilience is positively related to career commitment, underscoring its importance in fostering positive work outcomes

| [24] | Stefany, T., & Pusparini, E. S. (2023). Resilience and career commitment on millennial employee: a moderated mediation model of work engagement and role modelling. In 7th Global Conference on Business, Management, and Entrepreneurship (GCBME 2022) (pp. 1185-1192). Atlantis Press. |

[24]

. Furthermore, a study

| [16] | Malchelosse, K., Houlfort, N., Lavoie, C. É., & Masson, R. (2024). The role of resilience and psychological needs satisfaction in the relationship between passion for work and work-life enrichment. Current Psychology, 43(7), 6640-6656. |

[16]

emphasized how resilience contributes to work-life enrichment, supporting the notion that personal resilience enhances performance. Another study

| [7] | Gong, L., Zhang, S., & Liu, Z. (2024). The impact of inclusive leadership on task performance: a moderated mediation model of resilience capacity and work meaningfulness. Baltic Journal of Management, 19(1), 36-51. |

[7]

highlighted the mediating role of resilience capacity in the impact of inclusive leadership on task performance, suggesting that resilience is pivotal for meaningful work. Additionally, the moderating effect of individual resilience in managing role transitions and conflicts, indicating its role in reducing work disengagement

| [15] | Liman, P., Xiu, W., Fan, L., Tingting, F., Huaruo, C., & Ya, W. (2021). The relationship between college students’ resilience and career decision-making difficulties: the mediating role of career adaptability. Psychology, 12, 872-886, https://doi.org/10.4236/psych.2021.126053 |

[15]

. Organisations that aim to improve in-role performance should consider fostering personal resilience and creating a work environment that promotes thriving, adaptability, and openness to experience. These findings highlight the critical role of personal resilience in improving the in-role performance of accounting personnel. Organisations should consider implementing strategies to cultivate resilience among employees, as it can lead to enhanced performance and overall well-being.

The research hypothesis two sought to examine a no significant correlation between motivation and the in-role performance of accounting personnel. The results revealed a significant and positive correlation between personal motivation and in-role performance. The result reveals that personal motivation significantly and positively correlates with in-role performance. The result also indicates a strong positive relationship between personal motivation and in-role performance. This underscores the importance of promoting personal motivation among accounting personnel to enhance their in-role performance. A study

| [22] | Rifa’i, A., Muchlis, M., & Susanto, B. F. (2024). Building meaningful work through inclusive leadership: the role of psychological safety. In International Conference of Business and Social Sciences (pp. 974-987). |

[22]

found that compensation and work motivation have a significant positive impact on job satisfaction, which in turn affects employee performance. However, compensation itself does not directly influence employee performance. Similarly,

| [23] | Sabastian, R. A. (2021). The influence of leadership style and motivation on employee performance. Almana: Jurnal Manajemen Dan Bisnis, 5(1), 116-125. |

[23]

studied and focused on the influence of leadership style and motivation on employee performance, emphasizing the significance of these factors in the management services division. The study specifically targeted female employees of Bank Jateng Syariah. A study explored the effects of intrinsic and extrinsic motivation on employee performance, with job satisfaction as an intervening variable

| [26] | Yusuf, M. (2021). The effects of the intrinsic motivation and extrinsic motivation on employee performance with job satisfaction as an intervening variable at PT. Alwi Assegaf Palembang. Mbia, 20(1), 18-31. |

[26]

. The study revealed that job satisfaction did not mediate the relationship between motivation and performance. Additionally, a study

| [11] | Jufrizen, J., & Pratiwi, S. (2021, November). The effect of organizational climate on employee job satisfaction with work ethics as a moderating variable. In Journal of International Conference Proceedings, 4(2), 217-231. Association of International Business and Professional Management. |

[11]

, investigated the moderating role of work motivation in the influence of organizational culture on organizational commitment and employee performance. The study highlighted the importance of motivation in enhancing employee performance through organizational culture. Lastly, a study

| [19] | Nurasniar, W. A. (2021). Employee performance improvement through competence and organizational culture with work motivation as a mediation variable. Aptisi Transactions on Management (Atm), 6(2), 121-131. |

[19]

, aimed to improve employee performance through competence, organizational culture, and work motivation. The study emphasized the novelty of focusing on these factors in enhancing employee performance. Overall, these studies collectively contribute to understanding the intricate relationship between motivation and employee performance, highlighting the importance of factors such as compensation, job satisfaction, leadership style, organizational culture, and work-family conflict in influencing employee performance.

The research hypothesis three sought to determine the assumption that there is no significant combined correlation of resilience and motivation on in-role performance accounting personnel. The correlation analysis result of the research hypothesis three on the combined correlation of personal resilience and motivation with in-role performance of accounting personnel, showed strong significance and positive correlation indicating that individuals with higher levels of personal resilience and motivation are more likely to perform well within their formal job roles. These results are in agreement with the findings of the previous researches that have highlighted the importance of these factors in predicting job performance. For example, a study

| [9] | Hartung, P. J., & Cadaret, M. C. (2017). Career adaptability: Changing self and situation for satisfaction and success. Psychology of career adaptability, employability and resilience, 15-28. |

[9]

, discussed the concept of personal resilience, motivation, career adaptability and its role in changing oneself and the situation for job satisfaction and career success. Their work suggests that individuals who are motivated to adapt in their careers are better able to navigate challenges and achieve their goals, which can lead to higher levels of performance in their roles. Similarly, another study

| [19] | Nurasniar, W. A. (2021). Employee performance improvement through competence and organizational culture with work motivation as a mediation variable. Aptisi Transactions on Management (Atm), 6(2), 121-131. |

[19]

examined the role of personal resilience, motivation and psychological needs satisfaction in the correlation between passion for work and work-life enrichment. Their findings suggest that individuals who are more resilient and satisfied in their careers are more likely to experience enrichment in their work and personal lives, which can contribute to higher levels of performance.