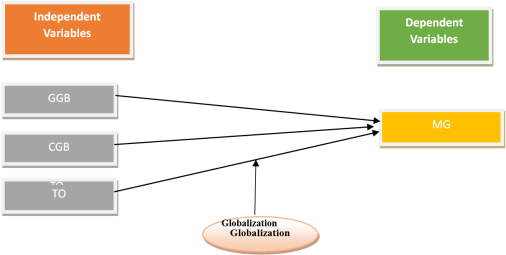

As more businesses and economies develop more concerns about environmental factors amidst social and governance, thereby shaping the financial flows, green finance had emerged as a critical tool for fostering sustainable manufacturing growth. Green finance had been embraced by developed economies in the achievement of sustainability. Thus, it became imperative for the Nigerian economy to promote sustainability in the manufacturing sector through the issuance, sale, and disbursement of green bonds. This study provided an analysis of how access to environmentally-friendly financial instruments drive manufacturing sector output in Nigeria with emphasis on the moderating role of globalization. The study examined the influence of green finance on the promotion of growth in the Nigerian manufacturing sector with specific focus on the role of globalization in the relationship between green finance and manufacturing sector growth. Data such as the contribution of the manufacturing sector to gross domestic product, government green bonds, corporate green bonds, and trade openness were collected from the Central Bank of Nigeria statistical bulletin and the World Development Index. Through the use of the Generalized Linear Regression (GLM), the study found that government green bonds had positive and significant influence on manufacturing sector growth. However, it was also found that corporate green bonds had negative but significant effect on manufacturing sector growth rate while globalization played negative but significant role in the relationship between green finance and manufacturing sector growth. It was recommended that strict measures at monitoring the green sector market should be enhanced while corporate green bonds should be encouraged in order to boost government’s contribution.

| Published in | Journal of Finance and Accounting (Volume 13, Issue 3) |

| DOI | 10.11648/j.jfa.20251303.14 |

| Page(s) | 125-142 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Green Finance, Green Bonds, Sustainability, Globalization

MG | GGB | CGB | INT | TO | |

|---|---|---|---|---|---|

Mean | 0.181256 | 3.670000 | 5.342857 | 11.29357 | 0.249322 |

Maximum | 0.298087 | 15.00000 | 22.40000 | 13.48000 | 0.279872 |

Minimum | 0.066999 | 0.000000 | 0.000000 | 9.490000 | 0.217515 |

Std. Dev. | 0.084477 | 6.390016 | 9.371385 | 1.680386 | 0.024801 |

Skewness | 0.195001 | 1.071637 | 1.115693 | 0.317600 | -0.229517 |

Kurtosis | 1.727358 | 2.310810 | 2.456040 | 1.648849 | 1.636865 |

Covariance Analysis: Ordinary | |||||

|---|---|---|---|---|---|

Correlation | |||||

Probability | MG | GGB | CGB | INT | TO |

MG | 1.000000 | ||||

----- | |||||

GGB | 0.340908 | 1.000000 | |||

0.4543 | ----- | ||||

CGB | -0.169875 | 0.244203 | 1.000000 | ||

0.7158 | 0.5977 | ----- | |||

INT | -0.371611 | -0.057130 | -0.267021 | 1.000000 | |

0.4118 | 0.9032 | 0.5627 | ----- | ||

TO | 0.212192 | 0.130164 | 0.704739 | -0.208100 | 1.000000 |

0.6478 | 0.7809 | 0.0770 | 0.6543 | ----- | |

Var | Level | First Difference | Stationarity | ||||

|---|---|---|---|---|---|---|---|

t-test | Cri-val | Prob | t-test | Cri-val | Prob | ||

MG | -2.70 | -3.52 | 0.1258 | -4.08 | -3.69 | 0.0353 | I (1) |

GGB | -2.98 | -3.52 | 0.0911 | -4.82 | -3.98 | 0.0020 | I (1) |

CGB | -5.44 | -3.69 | 0.0113 | - | - | - | I (0) |

INT | -6.07 | -3.69 | 0.0072 | - | - | - | I (0) |

TO | -3.89 | -3.69 | 0.0417 | - | - | - | I (0) |

Dependent Variable: D (MG) Method: Generalized Linear Model (Newton-Raphson / Marquardt steps) | ||||

|---|---|---|---|---|

Variable | Coefficient | Std. Error | z-Statistic | Prob. |

D (GGB) | 0.017502 | 0.003404 | 5.142197 | 0.0000 |

CGB | -0.013340 | 0.002745 | -4.860132 | 0.0000 |

INT | 0.053010 | 0.021886 | 2.422090 | 0.0154 |

TO | -1.815383 | 0.947730 | -1.915507 | 0.0554 |

Mean dependent var | 0.003350 | S.D. dependent var | 0.142023 | |

Sum squared resid | 0.004594 | Log likelihood | 11.71451 | |

Akaike info criterion | -2.571504 | Schwarz criterion | -2.710331 | |

Hannan-Quinn criter. | -3.127240 | Deviance | 0.004594 | |

Deviance statistic | 0.002297 | Pearson SSR | 0.004594 | |

Pearson statistic | 0.002297 | Dispersion | 0.002297 | |

GDP | Gross Domestic Product |

WDI | World Development Index |

UN | United Nations |

AfDB | African Development Bank |

SEC | Securities and Exchange Commission |

NGX | Nigerian Exchange Group |

TNP | The New Practice |

GHG | Globally Harmonized Gas |

ESG | Environmental, Social, and Governance |

PwC | PriceWaterouse Coopers |

GBP | Green Bonds Principles |

GLP | Green Loan Principles |

ICMA | International Capital Market Association |

SDGs | Sustainable Development Goals |

HSBC | Hongkong Shanghai Banking Corporation Limited |

OECD | Organization for Economic Cooperation and Development |

Year | MG | GGB | CGB | Int | TO | Med |

|---|---|---|---|---|---|---|

2017 | 0.120609 | 10.69 | 0 | 13.48 | 0.218033881 | 0 |

2018 | 0.215141 | 0 | 0 | 13.48 | 0.25170846 | 0 |

2019 | 0.298087 | 15 | 15 | 9.49 | 0.279872162 | 62.97124 |

2020 | 0.15219 | 0 | 0 | 9.49 | 0.217515096 | 0 |

2021 | 0.275056 | 0 | 0 | 10.365 | 0.242952656 | 0 |

2022 | 0.066999 | 0 | 22.4 | 11.375 | 0.272738838 | 0 |

2023 | 0.14071 | 0 | 0 | 11.375 | 0.262436352 | 0 |

MG | GGB | CGB | INT | TO | |

|---|---|---|---|---|---|

Mean | 0.181256 | 3.670000 | 5.342857 | 11.29357 | 0.249322 |

Median | 0.152190 | 0.000000 | 0.000000 | 11.37500 | 0.251708 |

Maximum | 0.298087 | 15.00000 | 22.40000 | 13.48000 | 0.279872 |

Minimum | 0.066999 | 0.000000 | 0.000000 | 9.490000 | 0.217515 |

Std. Dev. | 0.084477 | 6.390016 | 9.371385 | 1.680386 | 0.024801 |

Skewness | 0.195001 | 1.071637 | 1.115693 | 0.317600 | -0.229517 |

Kurtosis | 1.727358 | 2.310810 | 2.456040 | 1.648849 | 1.636865 |

Jarque-Bera | 0.516752 | 1.478343 | 1.538535 | 0.650151 | 0.603415 |

Probability | 0.772305 | 0.477509 | 0.463352 | 0.722473 | 0.739555 |

Sum | 1.268791 | 25.69000 | 37.40000 | 79.05500 | 1.745257 |

Sum Sq. Dev. | 0.042818 | 244.9938 | 526.9371 | 16.94219 | 0.003691 |

Observations | 7 | 7 | 7 | 7 | 7 |

Covariance Analysis: Ordinary, Date: 07/25/24, Time: 23:59, Sample: 2017 2023, Included observations: 7 Correlation | |||||

|---|---|---|---|---|---|

Probability | MG | GGB | CGB | INT | TO |

MG | 1.000000 | ||||

----- | |||||

GGB | 0.340908 | 1.000000 | |||

0.4543 | ----- | ||||

CGB | -0.169875 | 0.244203 | 1.000000 | ||

0.7158 | 0.5977 | ----- | |||

INT | -0.371611 | -0.057130 | -0.267021 | 1.000000 | |

0.4118 | 0.9032 | 0.5627 | ----- | ||

TO | 0.212192 | 0.130164 | 0.704739 | -0.208100 | 1.000000 |

0.6478 | 0.7809 | 0.0770 | 0.6543 | ----- | |

Null Hypothesis: MG has a unit root, Exogenous: Constant, Lag Length: 0 (Automatic - based on SIC, maxlag=1) | ||||

|---|---|---|---|---|

t-Statistic | Prob.* | |||

Augmented Dickey-Fuller test statistic | -2.700650 | 0.1258 | ||

Test critical values: | 1% level | -5.119808 | ||

5% level | -3.519595 | |||

10% level | -2.898418 | |||

*MacKinnon (1996) one-sided p-values. | ||||

Warning: Probabilities and critical values calculated for 20 observations | ||||

and may not be accurate for a sample size of 6 | ||||

Augmented Dickey-Fuller Test Equation | ||||

Dependent Variable: D (MG) | ||||

Method: Least Squares | ||||

Date: 07/25/24 Time: 23:59 | ||||

Sample (adjusted): 2018 2023 | ||||

Included observations: 6 after adjustments | ||||

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

MG (-1) | -1.261935 | 0.467271 | -2.700650 | 0.0541 |

C | 0.240611 | 0.095951 | 2.507651 | 0.0662 |

R-squared | 0.645814 | Mean dependent var | 0.003350 | |

Adjusted R-squared | 0.557268 | S.D. dependent var | 0.142023 | |

S.E. of regression | 0.094499 | Akaike info criterion | -1.619245 | |

Sum squared resid | 0.035721 | Schwarz criterion | -1.688658 | |

Log likelihood | 6.857734 | Hannan-Quinn criter. | -1.897113 | |

F-statistic | 7.293509 | Durbin-Watson stat | 1.833289 | |

Prob (F-statistic) | 0.054058 | |||

Null Hypothesis: D (MG) has a unit root, Exogenous: Constant, Lag Length: 0 (Automatic - based on SIC, maxlag=1) | ||||

|---|---|---|---|---|

t-Statistic | Prob.* | |||

Augmented Dickey-Fuller test statistic | -4.080201 | 0.0353 | ||

Test critical values: | 1% level | -5.604618 | ||

5% level | -3.694851 | |||

10% level | -2.982813 | |||

*MacKinnon (1996) one-sided p-values. | ||||

Warning: Probabilities and critical values calculated for 20 observations | ||||

and may not be accurate for a sample size of 5 | ||||

Augmented Dickey-Fuller Test Equation | ||||

Dependent Variable: D (MG, 2) | ||||

Method: Least Squares | ||||

Date: 07/26/24 Time: 00:00 | ||||

Sample (adjusted): 2019 2023 | ||||

Included observations: 5 after adjustments | ||||

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

D (MG (-1)) | -1.673090 | 0.410051 | -4.080201 | 0.0266 |

C | -0.022103 | 0.056666 | -0.390057 | 0.7225 |

R-squared | 0.847313 | Mean dependent var | -0.004164 | |

Adjusted R-squared | 0.796417 | S.D. dependent var | 0.279980 | |

S.E. of regression | 0.126327 | Akaike info criterion | -1.010704 | |

Sum squared resid | 0.047876 | Schwarz criterion | -1.166929 | |

Log likelihood | 4.526761 | Hannan-Quinn criter. | -1.429996 | |

F-statistic | 16.64804 | Durbin-Watson stat | 1.987504 | |

Prob (F-statistic) | 0.026587 | |||

Null Hypothesis: GGB has a unit root, Exogenous: Constant, Lag Length: 0 (Automatic - based on SIC, maxlag=1) | ||||

|---|---|---|---|---|

t-Statistic | Prob.* | |||

Augmented Dickey-Fuller test statistic | -2.977593 | 0.0911 | ||

Test critical values: | 1% level | -5.119808 | ||

5% level | -3.519595 | |||

10% level | -2.898418 | |||

*MacKinnon (1996) one-sided p-values. | ||||

Warning: Probabilities and critical values calculated for 20 observations | ||||

and may not be accurate for a sample size of 6 | ||||

Augmented Dickey-Fuller Test Equation | ||||

Dependent Variable: D (GGB) | ||||

Method: Least Squares | ||||

Date: 07/26/24 Time: 00:00 | ||||

Sample (adjusted): 2018 2023 | ||||

Included observations: 6 after adjustments | ||||

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

GGB (-1) | -1.280116 | 0.429916 | -2.977593 | 0.0408 |

C | 3.699363 | 3.232845 | 1.144306 | 0.3163 |

R-squared | 0.689105 | Mean dependent var | -1.781667 | |

Adjusted R-squared | 0.611381 | S.D. dependent var | 10.44251 | |

S.E. of regression | 6.509792 | Akaike info criterion | 6.845694 | |

Sum squared resid | 169.5096 | Schwarz criterion | 6.776280 | |

Log likelihood | -18.53708 | Hannan-Quinn criter. | 6.567826 | |

F-statistic | 8.866061 | Durbin-Watson stat | 1.642330 | |

Prob (F-statistic) | 0.040836 | |||

Null Hypothesis: D (GGB) has a unit root, Exogenous: Constant, Lag Length: 1 (Automatic - based on SIC, maxlag=1) | ||||

|---|---|---|---|---|

t-Statistic | Prob.* | |||

Augmented Dickey-Fuller test statistic | -2.818773 | 0.1302 | ||

Test critical values: | 1% level | -6.423637 | ||

5% level | -3.984991 | |||

10% level | -3.120686 | |||

*MacKinnon (1996) one-sided p-values. | ||||

Warning: Probabilities and critical values calculated for 20 observations | ||||

and may not be accurate for a sample size of 4 | ||||

Augmented Dickey-Fuller Test Equation | ||||

Dependent Variable: D (GGB, 2) | ||||

Method: Least Squares | ||||

Date: 07/26/24 Time: 00:01 | ||||

Sample (adjusted): 2020 2023 | ||||

Included observations: 4 after adjustments | ||||

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

D (GGB (-1)) | -2.153424 | 0.763958 | -2.818773 | 0.2170 |

D (GGB (-1), 2) | 0.351997 | 0.386690 | 0.910282 | 0.5299 |

C | -4.690712 | 2.959430 | -1.585005 | 0.3583 |

R-squared | 0.971218 | Mean dependent var | -3.750000 | |

Adjusted R-squared | 0.913653 | S.D. dependent var | 18.87459 | |

S.E. of regression | 5.546261 | Akaike info criterion | 6.377831 | |

Sum squared resid | 30.76101 | Schwarz criterion | 5.917551 | |

Log likelihood | -9.755661 | Hannan-Quinn criter. | 5.367782 | |

F-statistic | 16.87183 | Durbin-Watson stat | 0.975712 | |

Prob (F-statistic) | 0.169653 | |||

Null Hypothesis: CGB has a unit root, Exogenous: Constant, Lag Length: 1 (Automatic - based on SIC, maxlag=1) | ||||

|---|---|---|---|---|

t-Statistic | Prob.* | |||

Augmented Dickey-Fuller test statistic | -5.438372 | 0.0113 | ||

Test critical values: | 1% level | -5.604618 | ||

5% level | -3.694851 | |||

10% level | -2.982813 | |||

*MacKinnon (1996) one-sided p-values. | ||||

Warning: Probabilities and critical values calculated for 20 observations | ||||

and may not be accurate for a sample size of 5 | ||||

Augmented Dickey-Fuller Test Equation | ||||

Dependent Variable: D (CGB) | ||||

Method: Least Squares | ||||

Date: 07/26/24 Time: 00:01 | ||||

Sample (adjusted): 2019 2023 | ||||

Included observations: 5 after adjustments | ||||

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

CGB (-1) | -3.128792 | 0.575318 | -5.438372 | 0.0322 |

D (CGB (-1)) | 1.201405 | 0.416866 | 2.881992 | 0.1023 |

C | 18.02107 | 3.565667 | 5.054054 | 0.0370 |

R-squared | 0.963694 | Mean dependent var | 0.000000 | |

Adjusted R-squared | 0.927387 | S.D. dependent var | 19.06253 | |

S.E. of regression | 5.136724 | Akaike info criterion | 6.394417 | |

Sum squared resid | 52.77187 | Schwarz criterion | 6.160080 | |

Log likelihood | -12.98604 | Hannan-Quinn criter. | 5.765479 | |

F-statistic | 26.54346 | Durbin-Watson stat | 0.756106 | |

Prob (F-statistic) | 0.036306 | |||

Null Hypothesis: INT has a unit root, Exogenous: Constant, Lag Length: 1 (Automatic - based on SIC, maxlag=1) | ||||

|---|---|---|---|---|

t-Statistic | Prob.* | |||

Augmented Dickey-Fuller test statistic | -6.066488 | 0.0072 | ||

Test critical values: | 1% level | -5.604618 | ||

5% level | -3.694851 | |||

10% level | -2.982813 | |||

*MacKinnon (1996) one-sided p-values. | ||||

Warning: Probabilities and critical values calculated for 20 observations | ||||

and may not be accurate for a sample size of 5 | ||||

Augmented Dickey-Fuller Test Equation | ||||

Dependent Variable: D (INT) | ||||

Method: Least Squares | ||||

Date: 07/26/24 Time: 00:02 | ||||

Sample (adjusted): 2019 2023 | ||||

Included observations: 5 after adjustments | ||||

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

INT (-1) | -1.308262 | 0.215654 | -6.066488 | 0.0261 |

D (INT (-1)) | 0.428528 | 0.175399 | 2.443156 | 0.1345 |

C | 13.94097 | 2.386634 | 5.841268 | 0.0281 |

R-squared | 0.948457 | Mean dependent var | -0.421000 | |

Adjusted R-squared | 0.896913 | S.D. dependent var | 2.050587 | |

S.E. of regression | 0.658384 | Akaike info criterion | 2.285654 | |

Sum squared resid | 0.866940 | Schwarz criterion | 2.051316 | |

Log likelihood | -2.714134 | Hannan-Quinn criter. | 1.656716 | |

F-statistic | 18.40114 | Durbin-Watson stat | 2.087874 | |

Prob (F-statistic) | 0.051543 | |||

Null Hypothesis: TO has a unit root, Exogenous: Constant, Lag Length: 1 (Automatic - based on SIC, maxlag=1) | ||||

|---|---|---|---|---|

t-Statistic | Prob.* | |||

Augmented Dickey-Fuller test statistic | -3.893132 | 0.0417 | ||

Test critical values: | 1% level | -5.604618 | ||

5% level | -3.694851 | |||

10% level | -2.982813 | |||

*MacKinnon (1996) one-sided p-values. | ||||

Warning: Probabilities and critical values calculated for 20 observations | ||||

and may not be accurate for a sample size of 5 | ||||

Augmented Dickey-Fuller Test Equation | ||||

Dependent Variable: D (TO) | ||||

Method: Least Squares | ||||

Date: 07/26/24 Time: 00:02 | ||||

Sample (adjusted): 2019 2023 | ||||

Included observations: 5 after adjustments | ||||

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

TO (-1) | -2.360948 | 0.606439 | -3.893132 | 0.0601 |

D (TO (-1)) | 0.835079 | 0.367071 | 2.274978 | 0.1507 |

C | 0.590228 | 0.150438 | 3.923397 | 0.0592 |

R-squared | 0.895065 | Mean dependent var | 0.002146 | |

Adjusted R-squared | 0.790130 | S.D. dependent var | 0.039683 | |

S.E. of regression | 0.018179 | Akaike info criterion | -4.893338 | |

Sum squared resid | 0.000661 | Schwarz criterion | -5.127675 | |

Log likelihood | 15.23334 | Hannan-Quinn criter. | -5.522276 | |

F-statistic | 8.529705 | Durbin-Watson stat | 2.157073 | |

Prob (F-statistic) | 0.104935 | |||

Dependent Variable: D (MG), Method: Generalized Linear Model (Newton-Raphson / Marquardt steps), Date: 07/26/24 Time: 00:08, Sample (adjusted): 2018 2023, Included observations: 6 after adjustments, Family: Normal, Link: Identity Dispersion computed using Pearson Chi-Square Convergence achieved after 0 iterations Coefficient covariance computed using observed Hessian | ||||

|---|---|---|---|---|

Variable | Coefficient | Std. Error | z-Statistic | Prob. |

D (GGB) | 0.017502 | 0.003404 | 5.142197 | 0.0000 |

CGB | -0.013340 | 0.002745 | -4.860132 | 0.0000 |

INT | 0.053010 | 0.021886 | 2.422090 | 0.0154 |

TO | -1.815383 | 0.947730 | -1.915507 | 0.0554 |

Mean dependent var | 0.003350 | S.D. dependent var | 0.142023 | |

Sum squared resid | 0.004594 | Log likelihood | 11.71451 | |

Akaike info criterion | -2.571504 | Schwarz criterion | -2.710331 | |

Hannan-Quinn criter. | -3.127240 | Deviance | 0.004594 | |

Deviance statistic | 0.002297 | Pearson SSR | 0.004594 | |

Pearson statistic | 0.002297 | Dispersion | 0.002297 | |

Dependent Variable: D (MG), Method: Generalized Linear Model (Newton-Raphson / Marquardt steps), Date: 07/26/24 Time: 00:11, Sample (adjusted): 2018 2023, Included observations: 6 after adjustments, Family: Normal, Link: Identity Dispersion computed using Pearson Chi-Square Convergence achieved after 0 iterations Coefficient covariance computed using observed Hessian | ||||

|---|---|---|---|---|

Variable | Coefficient | Std. Error | z-Statistic | Prob. |

D (GGB) | 0.015758 | 0.003799 | 4.148122 | 0.0000 |

CGB | -0.012998 | 0.002751 | -4.725531 | 0.0000 |

INT | 0.061710 | 0.023406 | 2.636574 | 0.0084 |

TO | -2.269013 | 1.043883 | -2.173626 | 0.0297 |

MED | 0.001444 | 0.001429 | 1.010999 | 0.3120 |

Mean dependent var | 0.003350 | S.D. dependent var | 0.142023 | |

Sum squared resid | 0.002272 | Log likelihood | 12.24751 | |

Akaike info criterion | -2.415836 | Schwarz criterion | -2.589370 | |

Hannan-Quinn criter. | -3.110506 | Deviance | 0.002272 | |

Deviance statistic | 0.002272 | Pearson SSR | 0.002272 | |

Pearson statistic | 0.002272 | Dispersion | 0.002272 | |

| [1] | Al-Rodhan, N. R., & Stoudmann, G. (2006). Definitions of globalization: A comprehensive overview and a proposed definition. Program on the geopolitical implications of globalization and transnational security, 6(1-21). |

| [2] | Efosa, I. O., James, A. O., & Joseph, D. I. E. Impact of Green Finance on Green Infrastructure Development in Nigeria (1995–2022). Strategic Management Practices & Sustainable Development in a Global Economy, 273. |

| [3] | Inah, O. I., Abam, F. I., & Nwankwojike, B. N. (2022). Exploring the CO2 emissions drivers in the Nigerian manufacturing sector through decomposition analysis and the potential of carbon tax (CAT) policy on CO2 mitigation. Future Business Journal, 8(1), 61. |

| [4] | Jiakui, C., Abbas, J., Najam, H., Liu, J., & Abbas, J. (2023). Green technological innovation, green finance, and financial development and their role in green total factor productivity: Empirical insights from China. Journal of Cleaner Production, 382(135131), 1-8. |

| [5] | Larsson, T. (2001). The race to the top: The real story of globalization. US: Cato Institute. |

| [6] | Lindenberg, N. (2014). Definition of green finance. German Development Institute, 1-4. |

| [7] | Oguntuase, O. J., & Windapo, A. (2021). Green bonds and green buildings: New options for achieving sustainable development in Nigeria. Housing and SDGs in Urban Africa, 193-218. |

| [8] | Ouyand, H., Guan, C., & Yu, B. (2023). Green finance, natural resources, and economic growth: Theory analysis and empirical research. Resources Policy, 83(103604), 1-14. |

| [9] | Paramole, A. (2023). Promoting Environmental Sustainability in Nigeria through Green Bonds. |

| [10] | TNP (2024). The emergence of sustainable finance in the Nigerian capital market. Retrieved from |

| [11] |

Tufail, M., Song, L., & Khan, Z. (2024). Green finance and green growth nexus: evaluating the role of globalization and human capital. Journal of Applied Economics, 27(1), 2309437.

https://www.tandfonline.com/action/showCitFormats?doi=10.1080/15140326.2024.2309437 |

| [12] | Van Hamme, G., & Pion, G. (2012). The relevance of the world‐system approach in the era of globalization of economic flows and networks. Geografiska Annaler: Series B, Human Geography, 94(1), 65-82. |

| [13] | Wang, K. H., Zhao, Y. X., Jiang, C. F., & Li, Z. Z. (2022). Does green finance inspire sustainable development? Evidence from a global perspective. Economic Analysis and Policy, 75, 412-426. |

| [14] | Wang, M. L. (2023). Effects of green finance policy on the green innovation efficiency of the manufacturing industry: A difference-in-difference model. Technological Forecasting & Social Change, 189(122333), 1-10. |

| [15] | Wang, X., & Wang, Q. (2021). Research on the impact of green finance on the upgrading of China’s regional industrial structure from the perspective of sustainable development. Resource Policy, 74(102436), 1-10. |

| [16] | Martini, A. (2021). Socially responsible investing: from the ethical origins to the sustainable development framework of the European Union. Environment, development and sustainability, 23(11), 16874-16890. |

| [17] | Dzah, C., Agyapong, J. O., Apprey, M. W., Agbevanu, K. T. & Kagbetor, P. K. (2022). Assessment of perceptions and practices of electronic waste management among commercial consumers in Ho, Ghana. Sustainable Environment, 8(1), 1-16, |

| [18] | Banwo & Ighodalo (2024). Building a resilient future: leveraging board evaluation for enhanced performance and sustainability. Retrieved from |

| [19] | United Nations Development Organization (2022). United Nations Development Report 2022. The future of industrialization in a post-pandemic period. Retrieved from |

| [20] |

International Finance Corporation (2013). How IFC creates opportunity. Retrieved from

https://www.ifc.org/content/dam/ifc/doc/mgrt/ar2013-stories-of-impact.pdf |

| [21] | Spratt, S. & Griffith-Jones, S. (2013). Mobilising investment for inclusive green growth in low-income countries. BMZ Federal Ministry for Economic Cooperation and Development, 1-48. |

| [22] | Gilbert, N. (2012). Mapping of green finance. Delivered by IDFC Members in 2011, Ecofys. |

| [23] | Zadek and Flynn (2013). South-originating green finance: Exploring the potential. The Geneva International Finance Dialogues, UNEP FI, SDC, and iisd. |

| [24] | Pricewaterhouse Coopers Consultants (PWC) (2013): Exploring Green Finance Incentives in China, PWC. |

| [25] |

International Capital Market Association (2017) The green bond principles 2017: voluntary process guidelines for issuing green bonds. Annual Report. International Capital Market Association, Switzerland.

https://www.icmagroup.org/assets/documents/Regulatory/GreenBonds/-GreenBondsBrochure-JUNE2017.pdf Accessed 20 July 2019. |

| [26] | Filkova M, Frandon-Martinez C, Giorg A (2019) Green bonds: The state of the market 2018. Climate Bonds Initiative, London. |

| [27] | Wallerstein I (1974) The Modern World-System I: Capitalist Agriculture and the Origins of the European World-Economy in the Sixteenth Century. New York: Academic Press. |

| [28] | Frank AG and Gills B (eds) (1996) The World-System: Five Hundred or Five Thousand Years? New York: Routledge. |

| [29] | Sheikhazami, A., & Nikpour, Z. An Introduction to World-System Theory: With Emphasis on Social Development Planning Theories. |

| [30] | Appadurai, A. (1990). Disjuncture and difference in the global cultural economy. Public Culture, 2(2), 1-24. |

| [31] | Robertson, R. (1995). Globalization: Time-space and homogeneity-heterogeneity. In global modernities, ed. Mike Featherstone, Scott Lash and Roland Robertson. 24-44. London: Sage Publications. |

| [32] | Sharma, M., & Haldar, T. (2021). Cultural homogeneity and happiness: A cross-cultural study. The International Journal of Indian Psychology, 9(2), 1265-1278. |

| [33] | Aizenman, J., & Ito, H. (2020). The political-economy trilemma. Open Economies Review, 31(5), 945-975. |

| [34] | Friedmann, J. (2005). Globalization and the emerging culture of planning. Progress in Planning, 64(3), 183-234. |

| [35] | Gabriel, A. (2008). The meaning of theory. Sociological Theory 26, 173–199. |

| [36] | Zainudin, A. (2012). Analyzing the moderating variable in a model. A Handbook on SEM, Universiti Sultan Zainal Abidin. |

APA Style

Ushie, P. O., Demehin, A. J., Otapo, T. W., Dare, F. D. (2025). Green Finance and Manufacturing Sector Growth in Nigeria: The Role of Globalization. Journal of Finance and Accounting, 13(3), 125-142. https://doi.org/10.11648/j.jfa.20251303.14

ACS Style

Ushie, P. O.; Demehin, A. J.; Otapo, T. W.; Dare, F. D. Green Finance and Manufacturing Sector Growth in Nigeria: The Role of Globalization. J. Finance Account. 2025, 13(3), 125-142. doi: 10.11648/j.jfa.20251303.14

@article{10.11648/j.jfa.20251303.14,

author = {Paul Obogo Ushie and Adeniyi James Demehin and Toyin Waliu Otapo and Funso David Dare},

title = {Green Finance and Manufacturing Sector Growth in Nigeria: The Role of Globalization},

journal = {Journal of Finance and Accounting},

volume = {13},

number = {3},

pages = {125-142},

doi = {10.11648/j.jfa.20251303.14},

url = {https://doi.org/10.11648/j.jfa.20251303.14},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.jfa.20251303.14},

abstract = {As more businesses and economies develop more concerns about environmental factors amidst social and governance, thereby shaping the financial flows, green finance had emerged as a critical tool for fostering sustainable manufacturing growth. Green finance had been embraced by developed economies in the achievement of sustainability. Thus, it became imperative for the Nigerian economy to promote sustainability in the manufacturing sector through the issuance, sale, and disbursement of green bonds. This study provided an analysis of how access to environmentally-friendly financial instruments drive manufacturing sector output in Nigeria with emphasis on the moderating role of globalization. The study examined the influence of green finance on the promotion of growth in the Nigerian manufacturing sector with specific focus on the role of globalization in the relationship between green finance and manufacturing sector growth. Data such as the contribution of the manufacturing sector to gross domestic product, government green bonds, corporate green bonds, and trade openness were collected from the Central Bank of Nigeria statistical bulletin and the World Development Index. Through the use of the Generalized Linear Regression (GLM), the study found that government green bonds had positive and significant influence on manufacturing sector growth. However, it was also found that corporate green bonds had negative but significant effect on manufacturing sector growth rate while globalization played negative but significant role in the relationship between green finance and manufacturing sector growth. It was recommended that strict measures at monitoring the green sector market should be enhanced while corporate green bonds should be encouraged in order to boost government’s contribution.},

year = {2025}

}

TY - JOUR T1 - Green Finance and Manufacturing Sector Growth in Nigeria: The Role of Globalization AU - Paul Obogo Ushie AU - Adeniyi James Demehin AU - Toyin Waliu Otapo AU - Funso David Dare Y1 - 2025/06/30 PY - 2025 N1 - https://doi.org/10.11648/j.jfa.20251303.14 DO - 10.11648/j.jfa.20251303.14 T2 - Journal of Finance and Accounting JF - Journal of Finance and Accounting JO - Journal of Finance and Accounting SP - 125 EP - 142 PB - Science Publishing Group SN - 2330-7323 UR - https://doi.org/10.11648/j.jfa.20251303.14 AB - As more businesses and economies develop more concerns about environmental factors amidst social and governance, thereby shaping the financial flows, green finance had emerged as a critical tool for fostering sustainable manufacturing growth. Green finance had been embraced by developed economies in the achievement of sustainability. Thus, it became imperative for the Nigerian economy to promote sustainability in the manufacturing sector through the issuance, sale, and disbursement of green bonds. This study provided an analysis of how access to environmentally-friendly financial instruments drive manufacturing sector output in Nigeria with emphasis on the moderating role of globalization. The study examined the influence of green finance on the promotion of growth in the Nigerian manufacturing sector with specific focus on the role of globalization in the relationship between green finance and manufacturing sector growth. Data such as the contribution of the manufacturing sector to gross domestic product, government green bonds, corporate green bonds, and trade openness were collected from the Central Bank of Nigeria statistical bulletin and the World Development Index. Through the use of the Generalized Linear Regression (GLM), the study found that government green bonds had positive and significant influence on manufacturing sector growth. However, it was also found that corporate green bonds had negative but significant effect on manufacturing sector growth rate while globalization played negative but significant role in the relationship between green finance and manufacturing sector growth. It was recommended that strict measures at monitoring the green sector market should be enhanced while corporate green bonds should be encouraged in order to boost government’s contribution. VL - 13 IS - 3 ER -

Department of Finance, Adekunle Ajasin University, Akungba-Akoko, Nigeria

Information